All Activity

- Yesterday

-

Morryabie joined the community

Morryabie joined the community -

Avzqftwqmyb joined the community

Avzqftwqmyb joined the community -

Phuckyou99 joined the community

Phuckyou99 joined the community -

Dwfbhhzbdycc joined the community

Dwfbhhzbdycc joined the community -

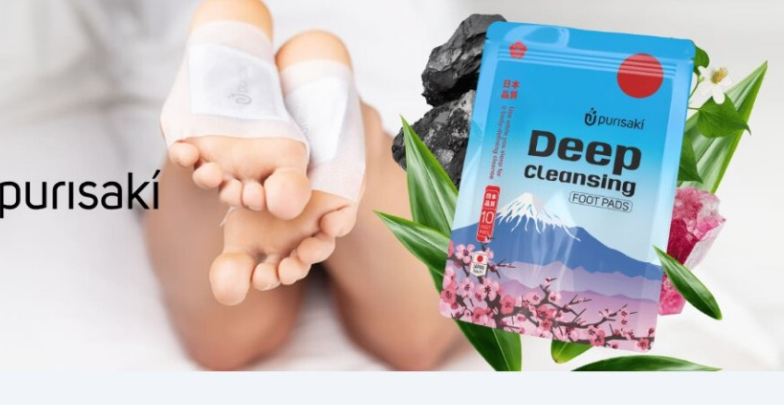

Glucotex: En omfattende guide til forståelse, anvendelse og betydning Glucotex Apotek er et navn, der i stigende grad dukker op i samtaler om sundhed, velvære og blodsukkerkontrol. I en tid, hvor livsstilssygdomme som diabetes og metabolisk syndrom er blevet mere udbredte, søger mange mennesker efter løsninger, der kan hjælpe med at opretholde en sund balance i kroppen. I denne artikel vil vi udforske, hvad Glucotex er, hvordan det menes at fungere, dets potentielle fordele, samt hvad man bør være opmærksom på, før man anvender det. Begrænset udgave – køb Glucotex nu! Hvad er Glucotex? Glucotex fup eller legitim? beskrives ofte som et kosttilskud, der er udviklet med henblik på at støtte kroppens naturlige regulering af blodsukkeret. Det markedsføres typisk til personer, der ønsker at forbedre deres metaboliske sundhed, reducere sukkertrang eller opretholde stabile energiniveauer gennem dagen. Produktet indeholder som regel en kombination af naturlige ingredienser, såsom planteekstrakter, vitaminer og mineraler, der hver især har været forbundet med forskellige sundhedsmæssige fordele. Sammensætningen kan variere afhængigt af producenten, men fælles for mange formuleringer er fokus på ingredienser, der traditionelt er blevet brugt til at understøtte blodsukkerkontrol. Hvordan virker Glucotex? Glucotex menes at arbejde gennem flere mekanismer i kroppen. Først og fremmest sigter det mod at støtte insulinfølsomheden. Insulin er et hormon, der hjælper med at transportere glukose fra blodet ind i cellerne, hvor det bruges som energi. Når kroppen bliver mindre følsom over for insulin, kan blodsukkerniveauet stige, hvilket på sigt kan føre til sundhedsproblemer. Derudover kan Glucotex formel til glukosestyring indeholde ingredienser, der hjælper med at: Reducere optagelsen af sukker i tarmen Forbedre kroppens evne til at bruge glukose effektivt Mindske inflammation, som ofte er forbundet med metaboliske ubalancer Understøtte vægtkontrol ved at reducere appetit og sukkertrang Det er vigtigt at bemærke, at selvom disse mekanismer lyder lovende, varierer effekten fra person til person, og videnskabelig dokumentation kan være begrænset afhængigt af det specifikke produkt. Typiske ingredienser i Glucotex Selvom formuleringen kan variere, indeholder mange Glucotex-produkter ingredienser som: Berberin Et naturligt plantealkaloid, der ofte fremhæves for sin evne til at understøtte blodsukkerregulering. Berberin har været genstand for flere studier og anses som en af de mere effektive naturlige forbindelser i denne sammenhæng. Kanel-ekstrakt Kanel er traditionelt blevet brugt til at hjælpe med at stabilisere blodsukkeret. Nogle undersøgelser tyder på, at det kan forbedre insulinfølsomheden. Chrom (krom) Et essentielt mineral, der spiller en rolle i kulhydratmetabolismen og kan hjælpe kroppen med at bruge insulin mere effektivt. Gymnema Sylvestre En plante, der ofte kaldes “sukkerødelæggeren”, fordi den kan reducere smagsoplevelsen af sødt og dermed mindske sukkertrang. Bitter melon En frugt, der anvendes i traditionel medicin og menes at have blodsukkersænkende egenskaber. Disse ingredienser arbejder ofte sammen i en synergistisk effekt for at støtte kroppens naturlige processer. Potentielle fordele ved Glucotex Brugere af Glucotex formel til blodsukker rapporterer ofte en række mulige fordele, herunder: 1. Stabilisering af blodsukker En af de primære grunde til at tage Glucotex er at opnå mere stabile blodsukkerniveauer, hvilket kan reducere energidyk og sukkercravings. 2. Øget energiniveau Når blodsukkeret er stabilt, oplever mange færre udsving i energiniveauet og føler sig mere fokuserede gennem dagen. 3. Vægtkontrol Ved at reducere sukkertrang og forbedre stofskiftet kan Glucotex potentielt støtte vægttab eller vægtvedligeholdelse. 4. Bedre metabolisk sundhed Langvarig brug kan muligvis bidrage til en generel forbedring af kroppens metaboliske funktioner. Begrænset udgave – køb Glucotex nu! Hvem kan have gavn af Glucotex? Glucotex kapsler Optimal glukosemetabolisme henvender sig typisk til: Personer med ustabilt blodsukker Dem, der oplever hyppig sukkertrang Mennesker, der ønsker at forbedre deres kost og livsstil Personer i risiko for metaboliske lidelser Det er dog vigtigt at understrege, at Glucotex ikke er en erstatning for medicinsk behandling, især ikke for personer med diagnosticeret diabetes. Mulige bivirkninger og forholdsregler Selvom Glucotex ofte markedsføres som et naturligt produkt, betyder det ikke, at det er helt uden bivirkninger. Nogle personer kan opleve: Maveproblemer Kvalme Hovedpine Interaktion med medicin Det er derfor vigtigt at konsultere en læge, før man begynder at tage Glucotex, især hvis man allerede tager medicin eller har en eksisterende helbredstilstand. Videnskabelig evidens Der findes en vis mængde forskning på individuelle ingredienser i Glucotex, såsom berberin og krom. Disse studier viser generelt lovende resultater, når det gælder blodsukkerkontrol. Dog er der ofte mangel på omfattende kliniske studier, der specifikt undersøger Glucotex som et samlet produkt. Det betyder, at mens ingredienserne kan have dokumenterede effekter, er det ikke altid sikkert, at produktet som helhed vil give de samme resultater. Glucotex og livsstil For at opnå de bedste resultater bør Glucotex kombineres med en sund livsstil. Dette inkluderer: En balanceret kost rig på fibre, proteiner og sunde fedtstoffer Regelmæssig motion Tilstrækkelig søvn Stresshåndtering Kosttilskud fungerer bedst som et supplement – ikke en erstatning – for sunde vaner. Markedsføring og forbrugerbevidsthed Glucotex Anmeldelser markedsføres ofte online med stærke påstande om hurtige resultater. Som forbruger er det vigtigt at være kritisk og undersøge produktet grundigt. Kig efter: Gennemsigtige ingredienslister Tredjepartstestning Kundeanmeldelser Producentens troværdighed Undgå produkter, der lover mirakuløse resultater uden videnskabelig dokumentation. Begrænset udgave – køb Glucotex nu! Konklusion Glucotex Kapsler Anmeldelser er et kosttilskud, der retter sig mod personer, der ønsker at forbedre deres blodsukkerkontrol og generelle metaboliske sundhed. Det indeholder ofte en kombination af naturlige ingredienser, der hver især kan have gavnlige egenskaber. Selvom mange brugere rapporterer positive erfaringer, er det vigtigt at have realistiske forventninger og forstå, at effekten kan variere. Glucotex bør ikke ses som en mirakelløsning, men snarere som et supplement til en sund livsstil. Før man begynder at bruge Glucotex, er det altid en god idé at rådføre sig med en sundhedsprofessionel, især hvis man har eksisterende helbredsproblemer. Ved at kombinere viden, ansvarlig brug og sunde vaner kan Glucotex muligvis være en del af en større strategi for bedre sundhed og velvære. https://www.facebook.com/GlucotexAnmeldelser/ https://www.facebook.com/groups/glucotexanmeldelser/ https://www.facebook.com/groups/glucotexkapsler/ https://www.facebook.com/groups/glucotexingredienser/ https://www.facebook.com/groups/glucotexpris/ https://www.facebook.com/groups/glucotexfordele/ https://www.facebook.com/groups/glucotexbivirkninger/ https://www.facebook.com/groups/glucotexapotek/ https://www.facebook.com/groups/glucotexblodsukkerkapsler/ Visit: https://www.kissnutra.com/nl/glucotex-review/ https://www.kissnutra.com/de/purisaki-berberin-pflaster/

Glucotex: En omfattende guide til forståelse, anvendelse og betydning Glucotex Apotek er et navn, der i stigende grad dukker op i samtaler om sundhed, velvære og blodsukkerkontrol. I en tid, hvor livsstilssygdomme som diabetes og metabolisk syndrom er blevet mere udbredte, søger mange mennesker efter løsninger, der kan hjælpe med at opretholde en sund balance i kroppen. I denne artikel vil vi udforske, hvad Glucotex er, hvordan det menes at fungere, dets potentielle fordele, samt hvad man bør være opmærksom på, før man anvender det. Begrænset udgave – køb Glucotex nu! Hvad er Glucotex? Glucotex fup eller legitim? beskrives ofte som et kosttilskud, der er udviklet med henblik på at støtte kroppens naturlige regulering af blodsukkeret. Det markedsføres typisk til personer, der ønsker at forbedre deres metaboliske sundhed, reducere sukkertrang eller opretholde stabile energiniveauer gennem dagen. Produktet indeholder som regel en kombination af naturlige ingredienser, såsom planteekstrakter, vitaminer og mineraler, der hver især har været forbundet med forskellige sundhedsmæssige fordele. Sammensætningen kan variere afhængigt af producenten, men fælles for mange formuleringer er fokus på ingredienser, der traditionelt er blevet brugt til at understøtte blodsukkerkontrol. Hvordan virker Glucotex? Glucotex menes at arbejde gennem flere mekanismer i kroppen. Først og fremmest sigter det mod at støtte insulinfølsomheden. Insulin er et hormon, der hjælper med at transportere glukose fra blodet ind i cellerne, hvor det bruges som energi. Når kroppen bliver mindre følsom over for insulin, kan blodsukkerniveauet stige, hvilket på sigt kan føre til sundhedsproblemer. Derudover kan Glucotex formel til glukosestyring indeholde ingredienser, der hjælper med at: Reducere optagelsen af sukker i tarmen Forbedre kroppens evne til at bruge glukose effektivt Mindske inflammation, som ofte er forbundet med metaboliske ubalancer Understøtte vægtkontrol ved at reducere appetit og sukkertrang Det er vigtigt at bemærke, at selvom disse mekanismer lyder lovende, varierer effekten fra person til person, og videnskabelig dokumentation kan være begrænset afhængigt af det specifikke produkt. Typiske ingredienser i Glucotex Selvom formuleringen kan variere, indeholder mange Glucotex-produkter ingredienser som: Berberin Et naturligt plantealkaloid, der ofte fremhæves for sin evne til at understøtte blodsukkerregulering. Berberin har været genstand for flere studier og anses som en af de mere effektive naturlige forbindelser i denne sammenhæng. Kanel-ekstrakt Kanel er traditionelt blevet brugt til at hjælpe med at stabilisere blodsukkeret. Nogle undersøgelser tyder på, at det kan forbedre insulinfølsomheden. Chrom (krom) Et essentielt mineral, der spiller en rolle i kulhydratmetabolismen og kan hjælpe kroppen med at bruge insulin mere effektivt. Gymnema Sylvestre En plante, der ofte kaldes “sukkerødelæggeren”, fordi den kan reducere smagsoplevelsen af sødt og dermed mindske sukkertrang. Bitter melon En frugt, der anvendes i traditionel medicin og menes at have blodsukkersænkende egenskaber. Disse ingredienser arbejder ofte sammen i en synergistisk effekt for at støtte kroppens naturlige processer. Potentielle fordele ved Glucotex Brugere af Glucotex formel til blodsukker rapporterer ofte en række mulige fordele, herunder: 1. Stabilisering af blodsukker En af de primære grunde til at tage Glucotex er at opnå mere stabile blodsukkerniveauer, hvilket kan reducere energidyk og sukkercravings. 2. Øget energiniveau Når blodsukkeret er stabilt, oplever mange færre udsving i energiniveauet og føler sig mere fokuserede gennem dagen. 3. Vægtkontrol Ved at reducere sukkertrang og forbedre stofskiftet kan Glucotex potentielt støtte vægttab eller vægtvedligeholdelse. 4. Bedre metabolisk sundhed Langvarig brug kan muligvis bidrage til en generel forbedring af kroppens metaboliske funktioner. Begrænset udgave – køb Glucotex nu! Hvem kan have gavn af Glucotex? Glucotex kapsler Optimal glukosemetabolisme henvender sig typisk til: Personer med ustabilt blodsukker Dem, der oplever hyppig sukkertrang Mennesker, der ønsker at forbedre deres kost og livsstil Personer i risiko for metaboliske lidelser Det er dog vigtigt at understrege, at Glucotex ikke er en erstatning for medicinsk behandling, især ikke for personer med diagnosticeret diabetes. Mulige bivirkninger og forholdsregler Selvom Glucotex ofte markedsføres som et naturligt produkt, betyder det ikke, at det er helt uden bivirkninger. Nogle personer kan opleve: Maveproblemer Kvalme Hovedpine Interaktion med medicin Det er derfor vigtigt at konsultere en læge, før man begynder at tage Glucotex, især hvis man allerede tager medicin eller har en eksisterende helbredstilstand. Videnskabelig evidens Der findes en vis mængde forskning på individuelle ingredienser i Glucotex, såsom berberin og krom. Disse studier viser generelt lovende resultater, når det gælder blodsukkerkontrol. Dog er der ofte mangel på omfattende kliniske studier, der specifikt undersøger Glucotex som et samlet produkt. Det betyder, at mens ingredienserne kan have dokumenterede effekter, er det ikke altid sikkert, at produktet som helhed vil give de samme resultater. Glucotex og livsstil For at opnå de bedste resultater bør Glucotex kombineres med en sund livsstil. Dette inkluderer: En balanceret kost rig på fibre, proteiner og sunde fedtstoffer Regelmæssig motion Tilstrækkelig søvn Stresshåndtering Kosttilskud fungerer bedst som et supplement – ikke en erstatning – for sunde vaner. Markedsføring og forbrugerbevidsthed Glucotex Anmeldelser markedsføres ofte online med stærke påstande om hurtige resultater. Som forbruger er det vigtigt at være kritisk og undersøge produktet grundigt. Kig efter: Gennemsigtige ingredienslister Tredjepartstestning Kundeanmeldelser Producentens troværdighed Undgå produkter, der lover mirakuløse resultater uden videnskabelig dokumentation. Begrænset udgave – køb Glucotex nu! Konklusion Glucotex Kapsler Anmeldelser er et kosttilskud, der retter sig mod personer, der ønsker at forbedre deres blodsukkerkontrol og generelle metaboliske sundhed. Det indeholder ofte en kombination af naturlige ingredienser, der hver især kan have gavnlige egenskaber. Selvom mange brugere rapporterer positive erfaringer, er det vigtigt at have realistiske forventninger og forstå, at effekten kan variere. Glucotex bør ikke ses som en mirakelløsning, men snarere som et supplement til en sund livsstil. Før man begynder at bruge Glucotex, er det altid en god idé at rådføre sig med en sundhedsprofessionel, især hvis man har eksisterende helbredsproblemer. Ved at kombinere viden, ansvarlig brug og sunde vaner kan Glucotex muligvis være en del af en større strategi for bedre sundhed og velvære. https://www.facebook.com/GlucotexAnmeldelser/ https://www.facebook.com/groups/glucotexanmeldelser/ https://www.facebook.com/groups/glucotexkapsler/ https://www.facebook.com/groups/glucotexingredienser/ https://www.facebook.com/groups/glucotexpris/ https://www.facebook.com/groups/glucotexfordele/ https://www.facebook.com/groups/glucotexbivirkninger/ https://www.facebook.com/groups/glucotexapotek/ https://www.facebook.com/groups/glucotexblodsukkerkapsler/ Visit: https://www.kissnutra.com/nl/glucotex-review/ https://www.kissnutra.com/de/purisaki-berberin-pflaster/ -

Glucotex: En omfattende guide til forståelse, anvendelse og betydning Officielle side: https://www.kissnutra.com/da/glucotex-anmeldelser/ https://scribehow.com/page/Glucotex_Kapsler_Anmeldelser_Sandheden_om_Blodsukker_Glucotex_Kapsler__ZV1oqyHmSg-Dtm0MutRglw https://scribehow.com/page/Glucotex_Hvordan_Kapsler_Kan_Hjaelpe_med_Optimal_Glukosemetabolisme__ZnnUYLIxSL-22QG8_56tcw https://open.firstory.me/story/cmmyqs6y102o001ys19zx49au https://open.firstory.me/story/cmmyqvg5n02os01ys2nh9d3v7 https://soundcloud.com/aryan-miglani-267981311/glucotex-hvordan-kapsler-kan? https://soundcloud.com/aryan-miglani-267981311/glucotex-pris-og-kob-fa-det I en moderne verden, hvor livsstilen ofte er præget af stillesiddende arbejde, stress og en kost rig på raffinerede kulhydrater, oplever mange mennesker udfordringer med deres blodsukkerbalance. Ustabile blodsukkerniveauer kan føre til træthed, vægtøgning, sukkertrang og i nogle tilfælde udvikling af metaboliske sygdomme. Derfor er der opstået en stigende interesse for naturlige kosttilskud, der kan støtte kroppens egen regulering af glukose. Et af disse kosttilskud er Glucotex, som er blevet markedsført som en naturlig løsning til at understøtte blodsukker og energiniveau. I denne artikel vil vi gennemgå, hvad Glucotex er, hvordan det virker, dets ingrediener, fordele, brug, mulige bivirkninger og meget mere. Hvad er Glucotex? Glucotex Anmeldelser er et kosttilskud i kapselform, der er designet til at støtte kroppens naturlige evne til at regulere blodsukkeret og opretholde en sund metabolisk balance. Produktet henvender sig primært til voksne, der ønsker at forbedre deres energiniveau, reducere udsving i blodsukkeret og understøtte kroppens insulinrespons. Glucotex indeholder typisk en blanding af plantebaserede ingredienser og mikronæringsstoffer, som arbejder sammen for at støtte glukosemetabolismen. Det er vigtigt at understrege, at Glucotex ikke er medicin, men et supplement, der bør anvendes som en del af en sund livsstil. Facebook: https://www.facebook.com/GlucotexAnmeldelser/ https://www.facebook.com/groups/glucotexanmeldelser/ https://www.facebook.com/groups/glucotexkapsler/ https://www.facebook.com/groups/glucotexingredienser/ https://www.facebook.com/groups/glucotexpris/ https://www.facebook.com/groups/glucotexfordele/ https://www.facebook.com/groups/glucotexbivirkninger/ https://www.facebook.com/groups/glucotexapotek/ https://www.facebook.com/groups/glucotexblodsukkerkapsler/ Pinterest: https://in.pinterest.com/pin/978547825301658863 https://in.pinterest.com/pin/978547825301658901/ https://in.pinterest.com/pin/1145181011522721948 https://in.pinterest.com/pin/1145181011522721970 Videos: https://soundcloud.com/aryan-miglani-267981311/glucotex-hvordan-kapsler-kan? https://soundcloud.com/aryan-miglani-267981311/glucotex-pris-og-kob-fa-det https://vimeo.com/1175440367 https://videa.hu/videok/gasztro/glucotex-tabletter-til-blodsukkerregulering-effektiv-EsTMVqw5RNeKGu0P https://www.youtube.com/watch?v=PHXz5WC9TEk https://www.dailymotion.com/video/xa2sncc https://www.bilibili.tv/en/video/4798915327432704 https://slaps.com/track/2dP3BB3C Læs også: https://x.com/PiyushShar30511/status/2034924902483120373 https://www.instagram.com/p/DWGit87GQrZ/ https://www.threads.com/@kristinoem08/post/DWGiwpoEfyZ https://gettr.com/post/p3ydr80c024 https://hackmd.io/@glucotexpris/GlucotexKapsler https://groups.google.com/g/glucotexreview/c/Q8Ar0ZGQKxs https://medium.com/@glucotexanmeldelser/glucotex-oplevelse-og-resultater-hvad-brugere-siger-i-forum-f553eb6f885c https://glucotexanmeldelser.blogspot.com/2026/03/glucotex-kapsler-anmeldelser-officielle.html https://hackmd.io/@glucotexpris/glucotexanmeldelser https://impact-fitness-studio.blogspot.com/2026/03/glucotex-kapsler-anmeldelser-sandheden.html https://writer.dek-d.com/dek-d/writer/view.php?id=2671010 https://differ.blog/p/glucotex-oplevelse-og-resultater-hvad-brugere-siger-i-forum-8434bd Besøg: https://www.kissnutra.com/nl/glucotex-review/ https://www.kissnutra.com/de/purisaki-berberin-pflaster/ Tag: #Glucotex #GlucotexAnmeldelser #GlucotexKapsler #GlucotexPris #GlucotexKøb #GlucotexIngredienser #GlucotexFordele #GlucotexBivirkninger #GlucotexOplevelse #GlucotexBlodsukkerKapsler #GlucotexKosttilskud #GlucotexResultater #GlucotexAmazon #GlucotexForum #GlucotexTabletter #GlucotexTilBlodsukkerregulering #GlucotexUdtalelser #GlucotexOfficielleHjemmeside #GlucotexApotek #GlucotexFupEllerLegitim #GlucotexFormelTilGlukosestyring #GlucotexFormelTilBlodsukker #GlucotexKapslerOptimalGlukosemetabolisme

-

glucotexanmeldelser joined the community

-

Qbdlkfzwivcc joined the community

Qbdlkfzwivcc joined the community -

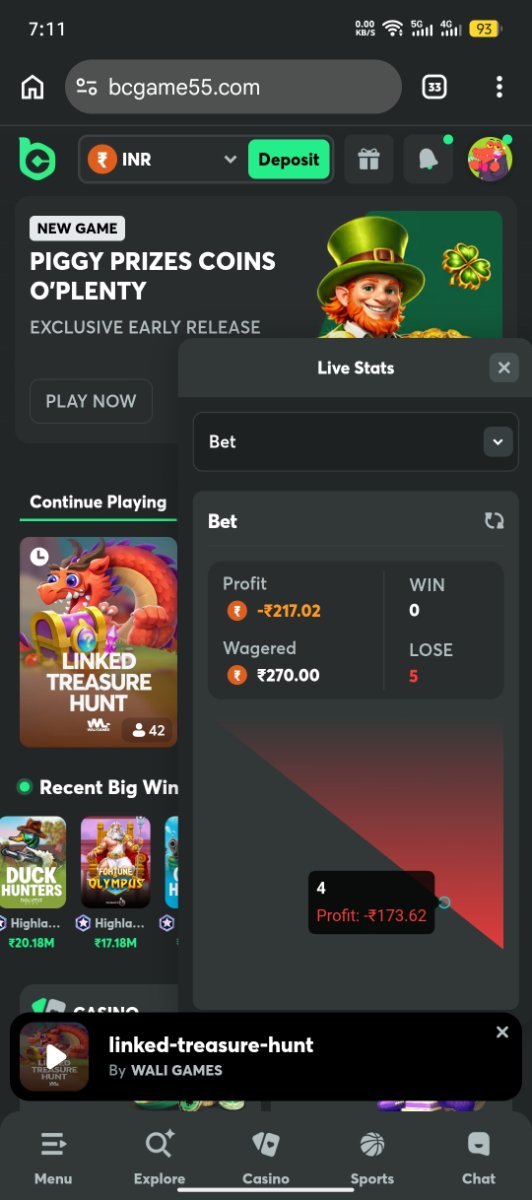

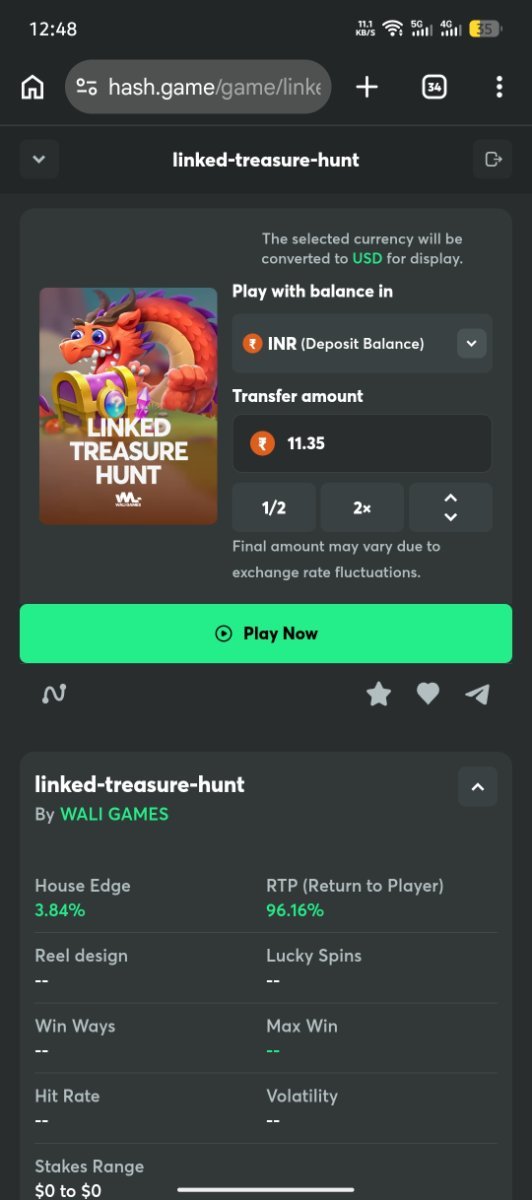

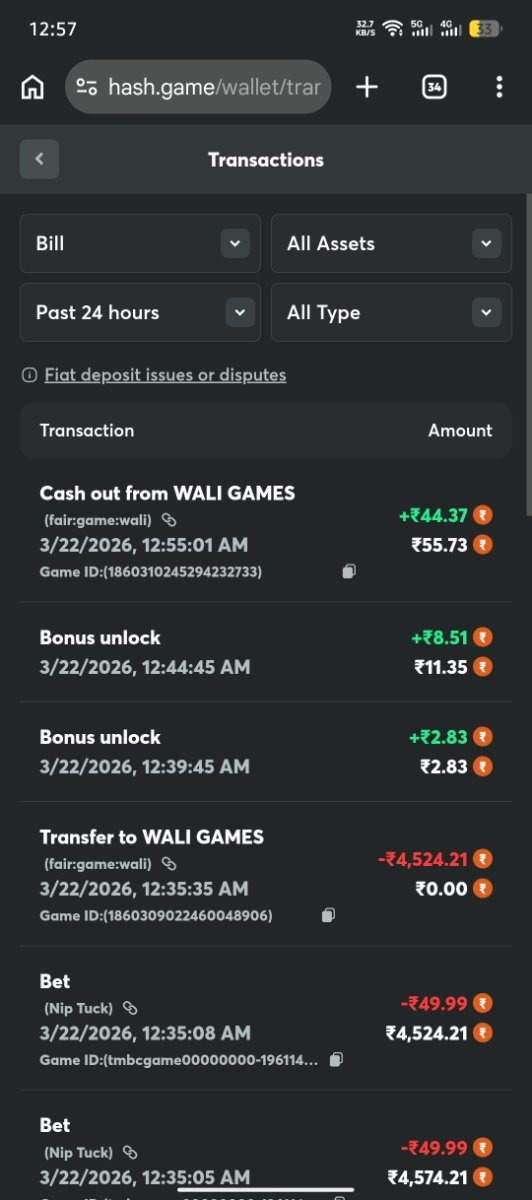

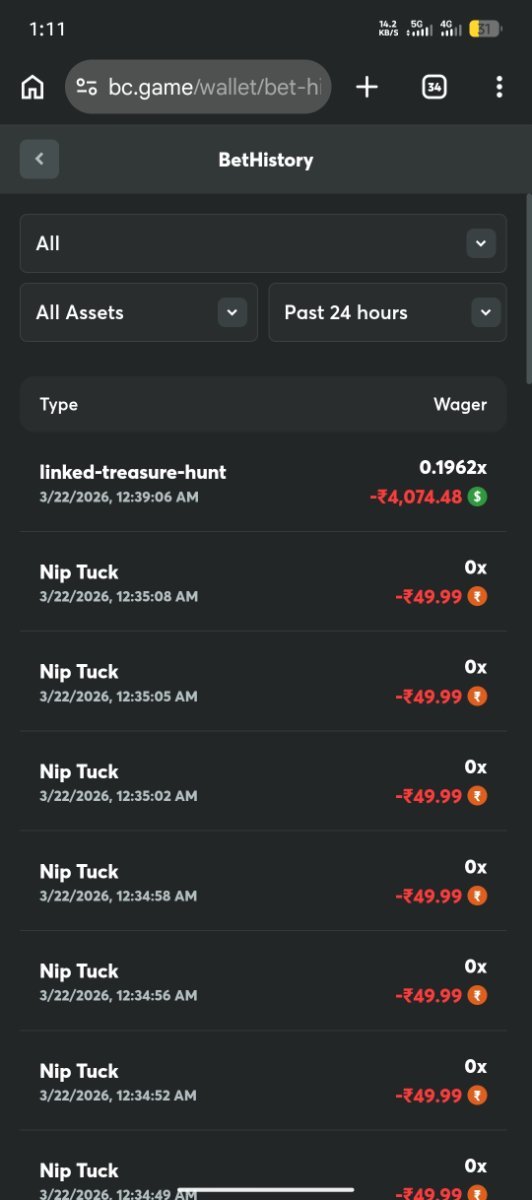

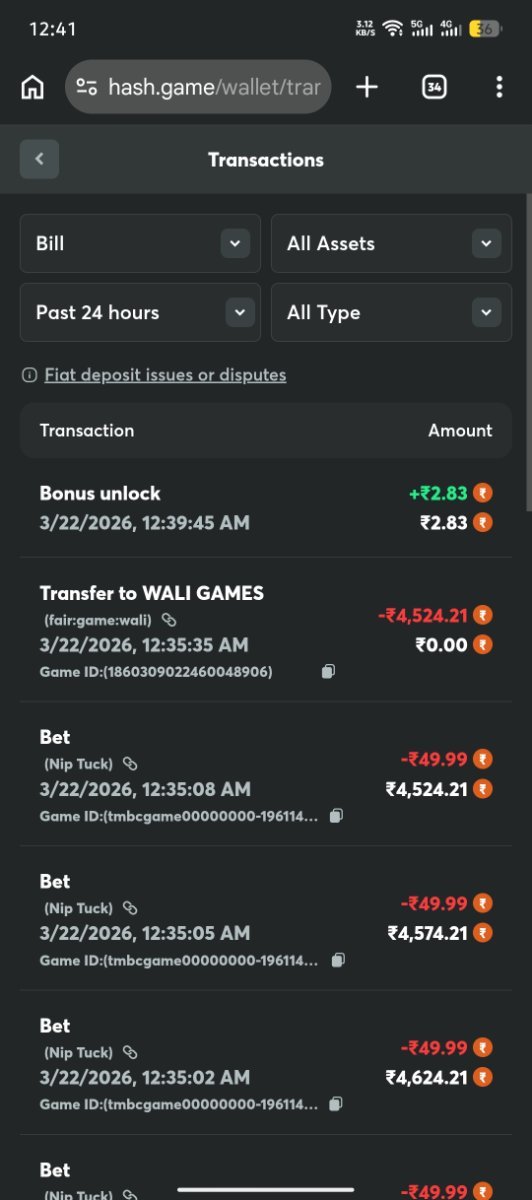

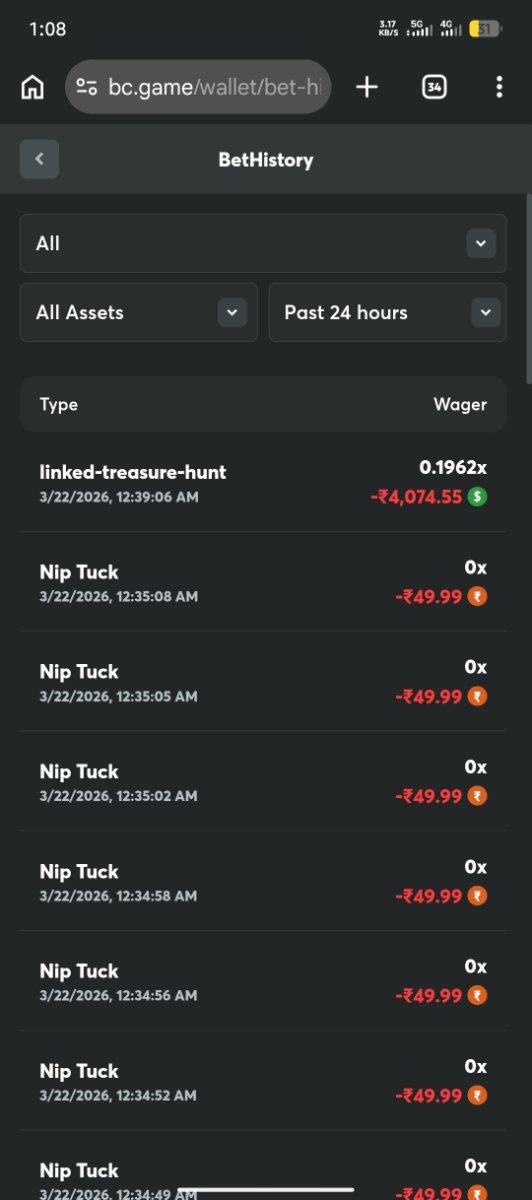

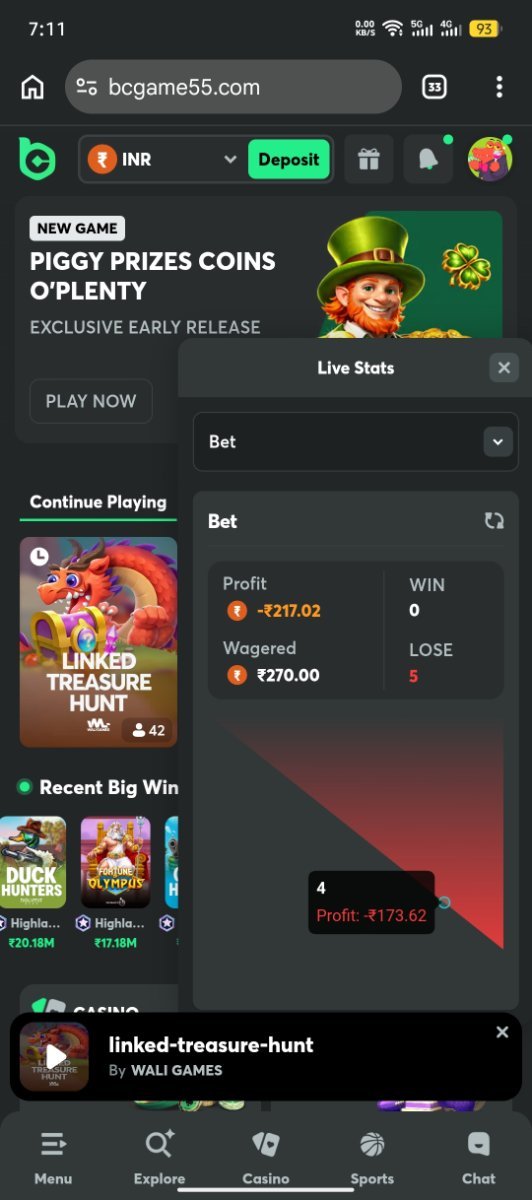

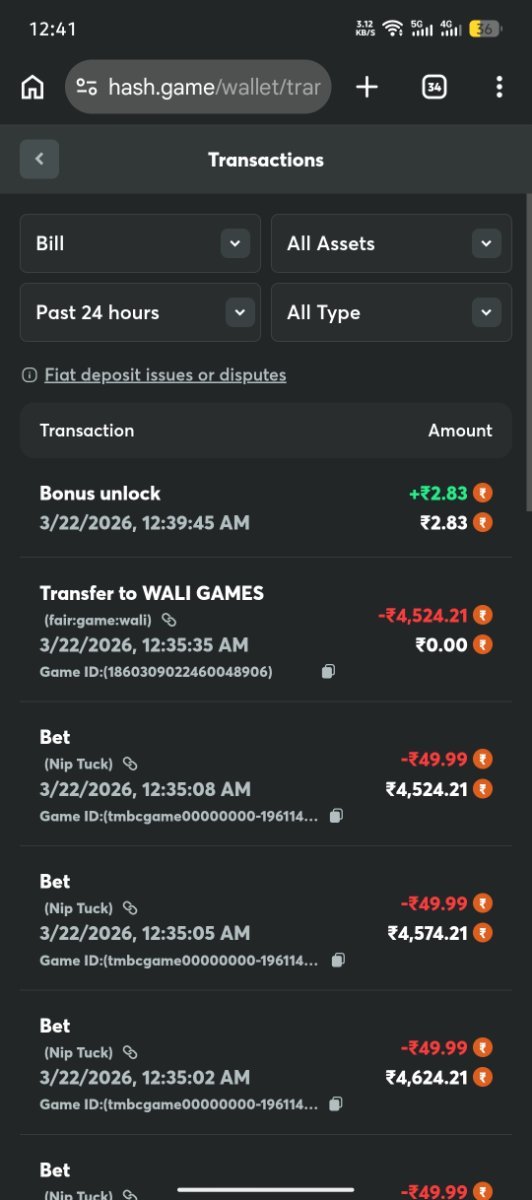

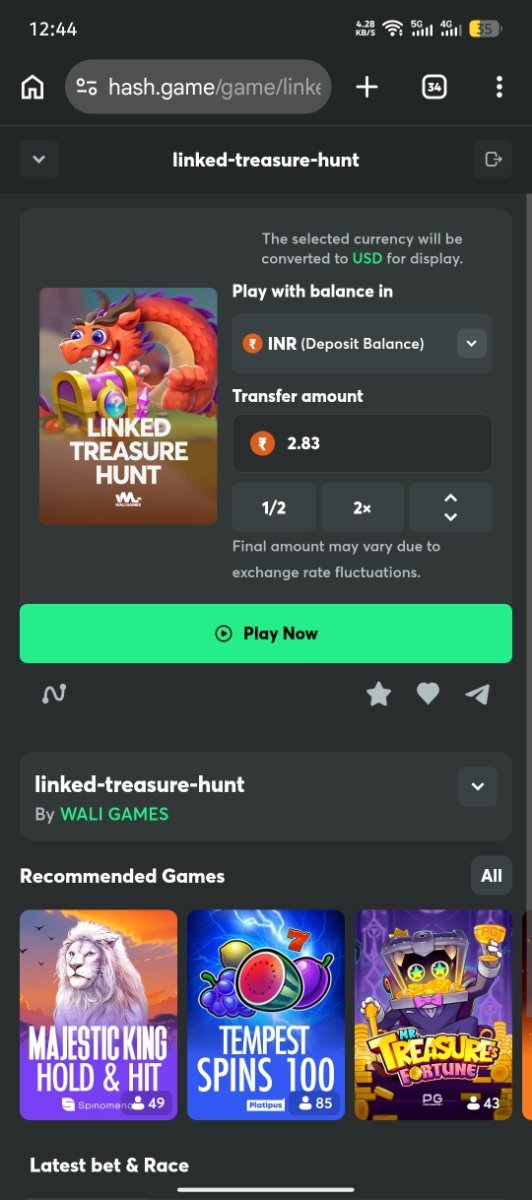

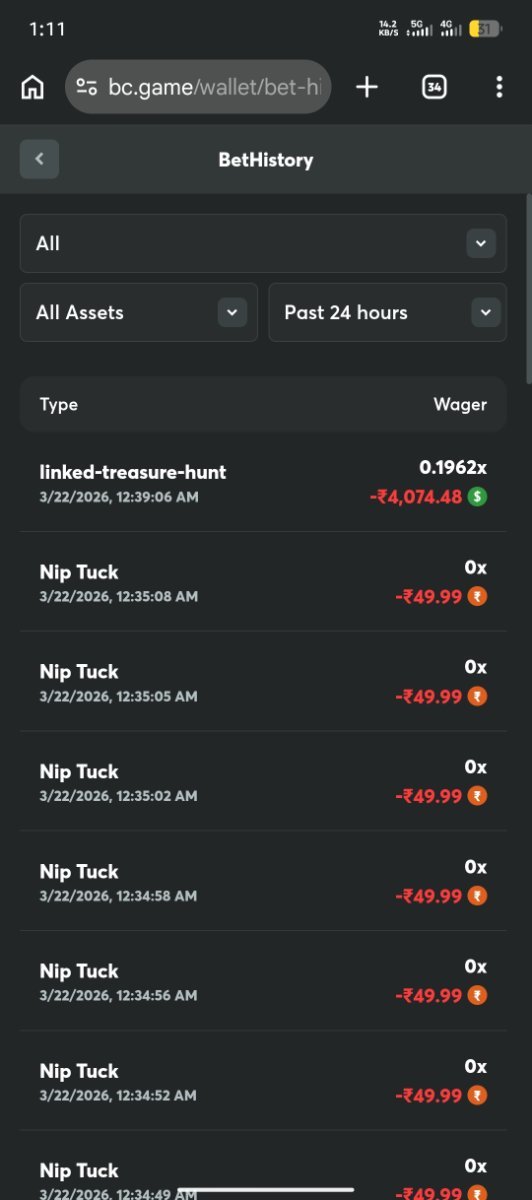

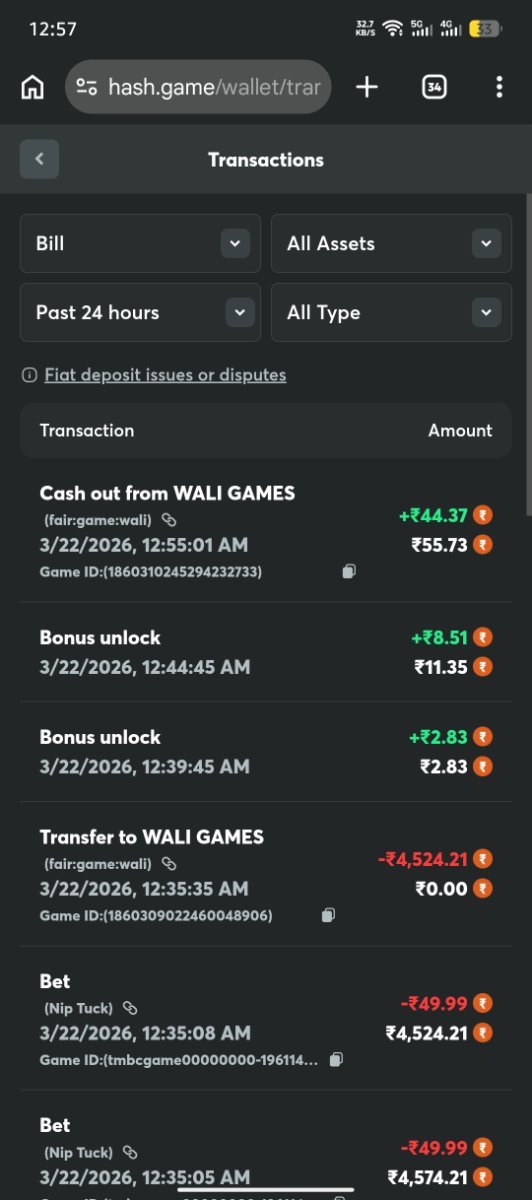

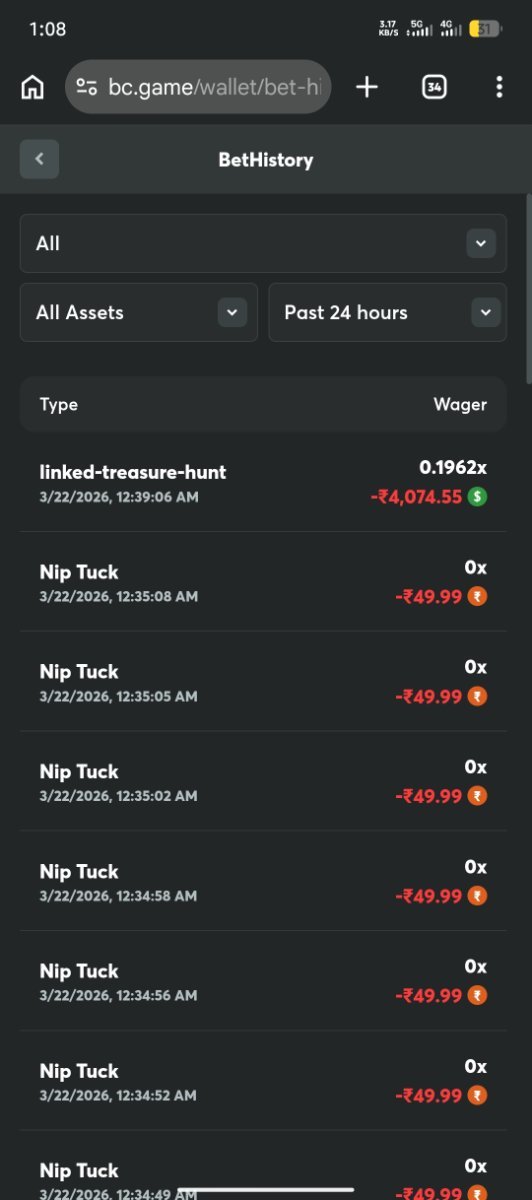

Hi, I am following up on my previous post. It has been over 24 hours and I have not received any response from support or moderators. As a VIP 25 Gold player, I am very disappointed with this delay. My balance (₹4,254.21) disappeared due to a glitch in Wali Games, and my Live Stats prove I didn't wager it. Please check my User ID: 61357425 and resolve this urgently. I have attached the proof again."

Hi, I am following up on my previous post. It has been over 24 hours and I have not received any response from support or moderators. As a VIP 25 Gold player, I am very disappointed with this delay. My balance (₹4,254.21) disappeared due to a glitch in Wali Games, and my Live Stats prove I didn't wager it. Please check my User ID: 61357425 and resolve this urgently. I have attached the proof again."

- Last week

-

lucashoegh123 joined the community

lucashoegh123 joined the community -

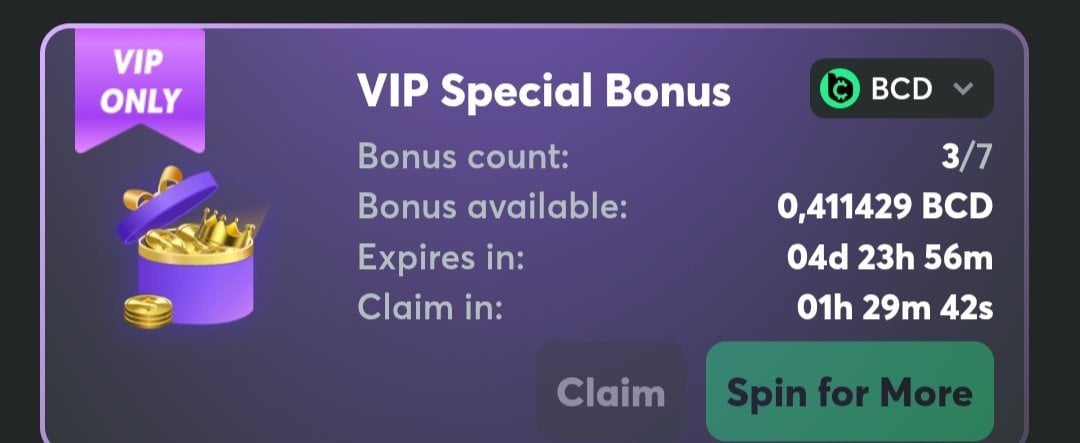

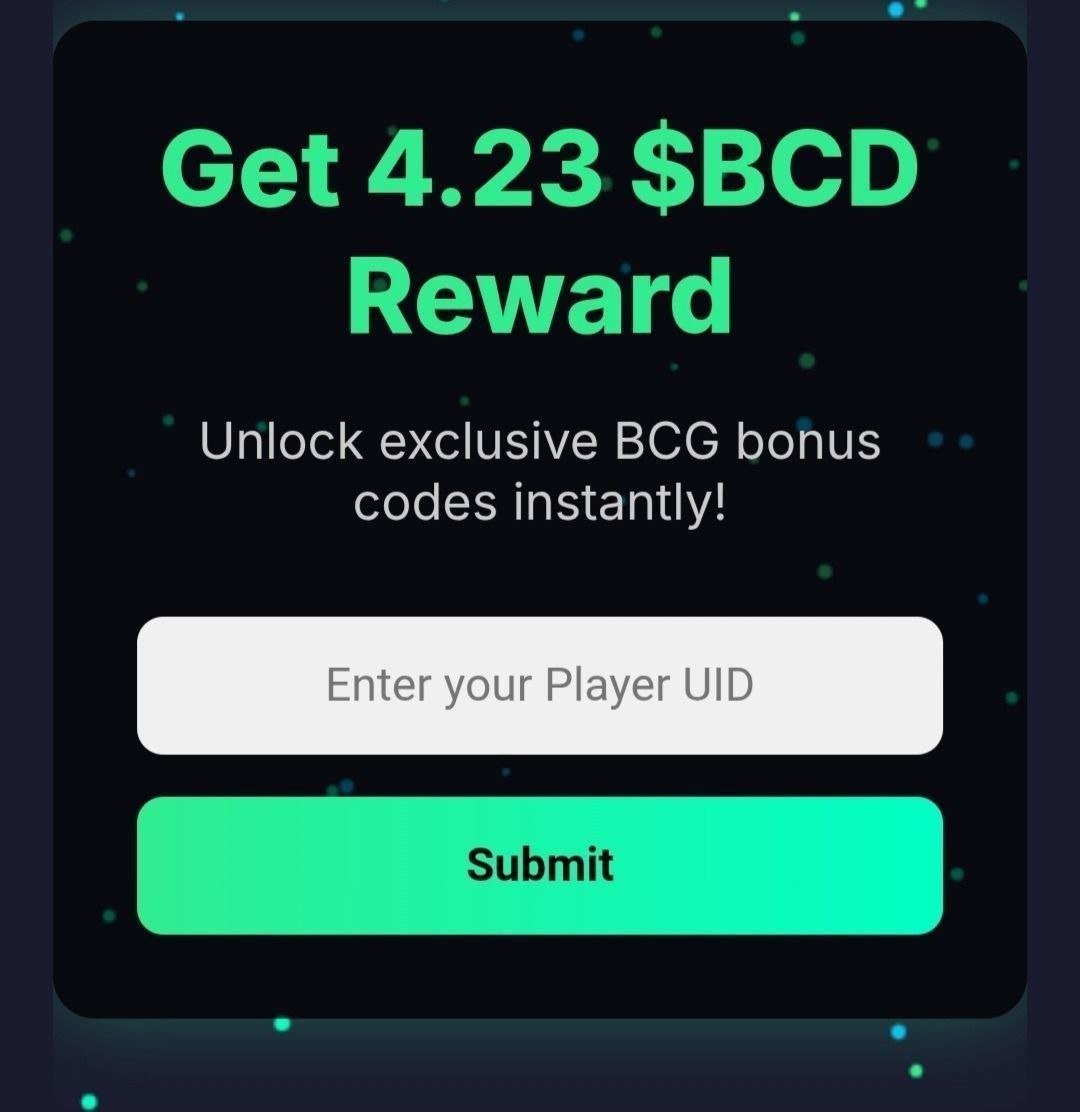

cocco code UPD : 4,23 $BCD Cocco Code valid For All players Lv

Swindows replied to Dann_BCGAME's topic in English

Scam? -

Hi, I am a VIP 25 Gold player (ID: 61357425). I encountered a technical glitch in the game 'Linked Treasure Hunt' by Wali Games. I transferred ₹4,524.21 to the game, but I only wagered ₹270 (as shown in my Live Stats). The remaining ₹4,254.21 disappeared and was never returned to my wallet. I have attached the proof showing that my total wagered amount is only ₹270. Please investigate this and refund my missing balance. User ID: 61357425 Transaction ID: 1860309022460048906

-

Jabirkv joined the community

-

KHOOWIN joined the community

KHOOWIN joined the community -

98260732 joined the community

98260732 joined the community -

Most people don’t think about their 401k until something forces them to. Maybe it’s a job change, a financial emergency, or that moment when you log in and realize your balance is finally “real money.” That is usually when questions start piling up Should I take a withdrawal? Can I move this account? What happens if I need the cash right now? If you’re dealing with any of those questions, you’re not alone. The topic of fidelity 401k withdrawal is one of the most searched and misunderstood areas in personal finance. And honestly, it’s easy to see why. Fidelity manages millions of retirement accounts, and while their platform is robust, it doesn’t automatically make decisions for you. That part is still on you. Whether you’re exploring fidelity 401k investments, thinking about a fidelity hardship withdrawal, or considering a fidelity 401k rollover, the impact of your decision can stretch decades into the future. So, let’s begin and learn more about it. What are the Fidelity 401k Withdrawal Rules? When people talk about fidelity 401k withdrawal, what they’re really asking is: When can I take my money without getting penalized? The answer depends heavily on timing. The age 59½ rule is the big one. Once you cross that threshold, you can withdraw funds from your 401k without the additional 10% early withdrawal penalty. Before that, things get more restrictive. If you take money out early, you’ll usually owe both income tax and that extra penalty. There are exceptions, though. One of the more useful ones is the “Rule of 55.” If you leave your job at age 55 or older, you may be able to access your 401k funds from that employer without the penalty. Then there’s the tax side of things, which often catches people off guard. Every fidelity investment 401k withdrawal is taxed as ordinary income. So, if you withdraw a large amount in one year, it could push you into a higher tax bracket. And later in life, required minimum distributions (RMDs) come into play. At a certain age, the IRS requires you to start withdrawing funds whether you need them or not. How to Withdraw from Fidelity 401k? Technically, initiating a fidelity 401k withdrawal online is simple. Log in, select your account, choose the withdrawal option, and follow the prompts. But the mechanics are the easy part the decisions behind them are where things get complicated. One of the most common missteps is withdrawing too much at once. It’s tempting, especially during major life events, to take a lump sum and “solve” the problem. Another issue is not considering alternatives. For example, if you’re switching jobs, a fidelity 401k rollover might be a better option than withdrawing funds outright. Timing also plays a subtle but important role. If markets are down and you withdraw funds, you’re essentially locking in losses. Fidelity 401k Investments: What Actually Drives Long-Term Growth? Your 401k isn’t just sitting there it’s working (or at least, it should be). The performance of your fidelity 401k investments plays a major role in how much you’ll have in retirement. Fidelity offers a mix of investment options, ranging from conservative bond funds to more aggressive stock-based portfolios. Many people default to target-date funds because they automatically adjust over time. The real question is how involved you want to be. If you prefer a hands-off approach, a diversified fund might make sense. Younger investors often lean toward growth-focused investments because they have time to ride out market fluctuations. As retirement gets closer, the focus usually shifts toward preserving capital. What’s interesting is that small adjustments over time can lead to significant differences in outcomes. When does Hardship Withdrawal Fidelity Makes Sense and When It Doesn’t? A hardship withdrawal fidelity option exists for a reason, but it’s not meant to be a go-to solution. These withdrawals are designed for specific situations: serious medical expenses, preventing foreclosure, funeral costs, or similar financial emergencies. You’ll need to provide documentation, and approval isn’t automatic. What makes a fidelity hardship withdrawal different is that it’s not just about accessing funds it’s about proving necessity. And once the money is withdrawn, it’s gone from your retirement account permanently. From a practical standpoint, this option should be treated as a last resort. Not because it’s bad but because it’s irreversible. That said, life happens. And when it does, having access to funds can make a real difference. The key is using this option carefully and only when truly needed. What You Need to Think Before Fidelity Investments Hardship Withdrawal? When considering a fidelity investments hardship withdrawal, it’s easy to focus on the immediate relief it provides. But it’s equally important to think about what comes next. Once the withdrawal is made, your account balance decreases not just by the amount you took, but by the potential growth that money could have generated over time. That’s the part many people overlook. One way to approach this is to have a recovery plan. If you do take a hardship withdrawal, consider increasing your contributions later to make up for the gap. Even small adjustments can help rebuild your savings over time. Another consideration is taxes. These withdrawals are still subject to income tax, which can add to the financial strain if not planned for properly. What are the Fidelity Investments 401k Withdrawal Options? There’s no one-size-fits-all approach to fidelity investments 401k withdrawal. Some people need immediate access to funds, while others are planning long-term income streams. A lump-sum withdrawal might make sense in a specific situation, but it often comes with higher taxes. Periodic withdrawals, on the other hand, can provide steady income while keeping taxes more manageable. Then there are required distributions later in life, which add another layer of planning. The key is aligning your withdrawal strategy with your overall financial goals. What works for one person might not work for another and that’s completely normal. Why Fidelity 401k Rollover is a Smart Move? A fidelity 401k rollover is often overlooked, but it can be one of the most effective ways to maintain control over your retirement savings. Instead of withdrawing funds and triggering taxes, you move them into another qualified account. The money stays invested, continues growing, and avoids immediate tax consequences. For many people, especially those changing jobs, this is the most practical option. It keeps your retirement plan intact while giving you more flexibility. How to Transfer 401k to Fidelity? To transfer 401k to Fidelity, you’ll typically open an account, initiate the transfer, and let Fidelity handle most of the coordination. A direct transfer is usually the safest route. It minimizes risk and avoids unnecessary complications. While the process can take a couple of weeks, it’s generally smooth if you follow the steps carefully. What are the Benefits of Fidelity Investments 401k Rollover? The benefits of a fidelity investments 401k rollover go beyond convenience. You gain better visibility, more investment options, and often lower fees. It also simplifies your financial life. Instead of tracking multiple accounts, everything is in one place. FAQ What is a fidelity 401k withdrawal? It’s the process of taking money out of your 401k account, usually subject to taxes and possible penalties. What qualifies for a hardship withdrawal fidelity? Situations like medical emergencies, foreclosure prevention, or funeral expenses. Is rolling over a 401k to Fidelity a good idea? Yes, in most cases it helps maintain tax advantages and simplifies account management. Can I transfer 401k to Fidelity anytime? Generally, yes transfer especially after leaving an employer.

Most people don’t think about their 401k until something forces them to. Maybe it’s a job change, a financial emergency, or that moment when you log in and realize your balance is finally “real money.” That is usually when questions start piling up Should I take a withdrawal? Can I move this account? What happens if I need the cash right now? If you’re dealing with any of those questions, you’re not alone. The topic of fidelity 401k withdrawal is one of the most searched and misunderstood areas in personal finance. And honestly, it’s easy to see why. Fidelity manages millions of retirement accounts, and while their platform is robust, it doesn’t automatically make decisions for you. That part is still on you. Whether you’re exploring fidelity 401k investments, thinking about a fidelity hardship withdrawal, or considering a fidelity 401k rollover, the impact of your decision can stretch decades into the future. So, let’s begin and learn more about it. What are the Fidelity 401k Withdrawal Rules? When people talk about fidelity 401k withdrawal, what they’re really asking is: When can I take my money without getting penalized? The answer depends heavily on timing. The age 59½ rule is the big one. Once you cross that threshold, you can withdraw funds from your 401k without the additional 10% early withdrawal penalty. Before that, things get more restrictive. If you take money out early, you’ll usually owe both income tax and that extra penalty. There are exceptions, though. One of the more useful ones is the “Rule of 55.” If you leave your job at age 55 or older, you may be able to access your 401k funds from that employer without the penalty. Then there’s the tax side of things, which often catches people off guard. Every fidelity investment 401k withdrawal is taxed as ordinary income. So, if you withdraw a large amount in one year, it could push you into a higher tax bracket. And later in life, required minimum distributions (RMDs) come into play. At a certain age, the IRS requires you to start withdrawing funds whether you need them or not. How to Withdraw from Fidelity 401k? Technically, initiating a fidelity 401k withdrawal online is simple. Log in, select your account, choose the withdrawal option, and follow the prompts. But the mechanics are the easy part the decisions behind them are where things get complicated. One of the most common missteps is withdrawing too much at once. It’s tempting, especially during major life events, to take a lump sum and “solve” the problem. Another issue is not considering alternatives. For example, if you’re switching jobs, a fidelity 401k rollover might be a better option than withdrawing funds outright. Timing also plays a subtle but important role. If markets are down and you withdraw funds, you’re essentially locking in losses. Fidelity 401k Investments: What Actually Drives Long-Term Growth? Your 401k isn’t just sitting there it’s working (or at least, it should be). The performance of your fidelity 401k investments plays a major role in how much you’ll have in retirement. Fidelity offers a mix of investment options, ranging from conservative bond funds to more aggressive stock-based portfolios. Many people default to target-date funds because they automatically adjust over time. The real question is how involved you want to be. If you prefer a hands-off approach, a diversified fund might make sense. Younger investors often lean toward growth-focused investments because they have time to ride out market fluctuations. As retirement gets closer, the focus usually shifts toward preserving capital. What’s interesting is that small adjustments over time can lead to significant differences in outcomes. When does Hardship Withdrawal Fidelity Makes Sense and When It Doesn’t? A hardship withdrawal fidelity option exists for a reason, but it’s not meant to be a go-to solution. These withdrawals are designed for specific situations: serious medical expenses, preventing foreclosure, funeral costs, or similar financial emergencies. You’ll need to provide documentation, and approval isn’t automatic. What makes a fidelity hardship withdrawal different is that it’s not just about accessing funds it’s about proving necessity. And once the money is withdrawn, it’s gone from your retirement account permanently. From a practical standpoint, this option should be treated as a last resort. Not because it’s bad but because it’s irreversible. That said, life happens. And when it does, having access to funds can make a real difference. The key is using this option carefully and only when truly needed. What You Need to Think Before Fidelity Investments Hardship Withdrawal? When considering a fidelity investments hardship withdrawal, it’s easy to focus on the immediate relief it provides. But it’s equally important to think about what comes next. Once the withdrawal is made, your account balance decreases not just by the amount you took, but by the potential growth that money could have generated over time. That’s the part many people overlook. One way to approach this is to have a recovery plan. If you do take a hardship withdrawal, consider increasing your contributions later to make up for the gap. Even small adjustments can help rebuild your savings over time. Another consideration is taxes. These withdrawals are still subject to income tax, which can add to the financial strain if not planned for properly. What are the Fidelity Investments 401k Withdrawal Options? There’s no one-size-fits-all approach to fidelity investments 401k withdrawal. Some people need immediate access to funds, while others are planning long-term income streams. A lump-sum withdrawal might make sense in a specific situation, but it often comes with higher taxes. Periodic withdrawals, on the other hand, can provide steady income while keeping taxes more manageable. Then there are required distributions later in life, which add another layer of planning. The key is aligning your withdrawal strategy with your overall financial goals. What works for one person might not work for another and that’s completely normal. Why Fidelity 401k Rollover is a Smart Move? A fidelity 401k rollover is often overlooked, but it can be one of the most effective ways to maintain control over your retirement savings. Instead of withdrawing funds and triggering taxes, you move them into another qualified account. The money stays invested, continues growing, and avoids immediate tax consequences. For many people, especially those changing jobs, this is the most practical option. It keeps your retirement plan intact while giving you more flexibility. How to Transfer 401k to Fidelity? To transfer 401k to Fidelity, you’ll typically open an account, initiate the transfer, and let Fidelity handle most of the coordination. A direct transfer is usually the safest route. It minimizes risk and avoids unnecessary complications. While the process can take a couple of weeks, it’s generally smooth if you follow the steps carefully. What are the Benefits of Fidelity Investments 401k Rollover? The benefits of a fidelity investments 401k rollover go beyond convenience. You gain better visibility, more investment options, and often lower fees. It also simplifies your financial life. Instead of tracking multiple accounts, everything is in one place. FAQ What is a fidelity 401k withdrawal? It’s the process of taking money out of your 401k account, usually subject to taxes and possible penalties. What qualifies for a hardship withdrawal fidelity? Situations like medical emergencies, foreclosure prevention, or funeral expenses. Is rolling over a 401k to Fidelity a good idea? Yes, in most cases it helps maintain tax advantages and simplifies account management. Can I transfer 401k to Fidelity anytime? Generally, yes transfer especially after leaving an employer. -

There is a moment that catches many people off guard. You have changed jobs, rolled over your old retirement savings, and now your money sits inside a Fidelity account. Everything feels organized until you need to use some of that money. That’s when the real question begins: how to withdraw money from fidelity 401k rollover without making an expensive mistake? It sounds simple on the surface. Log in, click withdraw, and transfer the funds. But retirement accounts don’t work like regular bank accounts. They come with rules, timelines, tax consequences, and if you are not careful penalties that can quietly eat into your savings. So, let’s begin and learn more about it. What a Fidelity 401(k) Rollover Really Means for Your Money? When your 401(k) is rolled over into an account with Fidelity Investments, it doesn’t suddenly become “free money” you can use anytime. It still carries the same purpose it always had funding your retirement. That means even though the account may now look like a regular investment account, it’s still governed by retirement rules. Taxes are deferred, growth continues, and withdrawals are monitored. This is where confusion usually starts. People assume that because they’ve left their job or completed a rollover, they now have unrestricted access. How to Withdraw Money from Fidelity 401k Rollover? If you log into your Fidelity dashboard, the process itself looks surprisingly simply. You’ll see your account, select the withdrawal option, enter the amount, and choose where the money should go. This is essentially what people mean when they search for how to withdraw money from Fidelity 401k withdrawal online. But here’s the part most guides skip: the platform won’t stop you from making a costly decision. It will process your request, but it’s up to you to understand the consequences behind it. Once you submit a withdrawal request, Fidelity may withhold a portion for taxes, and depending on your age and situation, additional penalties could apply. The money usually reaches your bank account within a few business days, but what you receive might be significantly less than what you requested. How to withdraw money from Fidelity 401k after leaving job? Leaving a job is often the turning point when people start thinking about withdrawals. If you’ve been wondering how to withdraw money from Fidelity 401k after leaving job, the key thing to know is that you now have control but also responsibility. You’re no longer tied to your employer’s plan rules, but you’re still bound by IRS guidelines. At this stage, many people feel tempted to cash out, especially if they need liquidity or want to simplify their finances. The reality, though, is that withdrawing immediately after leaving a job is rarely the most efficient option. Taxes and penalties can take a meaningful portion of your savings, and you lose the long-term growth that retirement accounts are designed for. In most cases, people either leave the funds where they are or roll them into an IRA. How to withdraw money from fidelity 401k before retirement There’s no denying it sometimes you need money earlier than planned. If you’re exploring how to withdraw money from fidelity 401k before retirement, it’s important to approach the decision with clarity. Yes, you can access your funds before age 59½, but doing so usually comes at a cost. That cost often includes a 10% early withdrawal penalty, along with regular income taxes. In practical terms, this means you could lose 20–30% (or more) of your withdrawal amount depending on your tax bracket. How to withdraw money from fidelity 401k without penalty This is one of the most common concerns people have. When searching for how to withdraw money from fidelity 401k without penalty, what they’re really asking is whether there’s a way to access their savings without losing a chunk of it. The answer depends largely on timing. Once you reach age 59½, withdrawals are generally penalty-free. Before that, you’ll need to qualify for specific exceptions. Another lesser-known approach involves structured withdrawals over time, sometimes referred to as substantially equal periodic payments. These require careful planning and long-term commitment, but they can help you avoid penalties if executed correctly. FAQ How to withdraw money from Fidelity 401k rollover easily? To withdraw money from fidelity 401k rollover, log in to your account with Fidelity Investments, go to your retirement account, select the withdrawal option, enter the amount, and choose your preferred transfer method. While the process is simple, you should review taxes and penalties before confirming. Can I withdraw money from my Fidelity 401(k) anytime? You can request a withdrawal, but whether you should depend on your age and situation. If you're under 59½, withdrawing early may result in taxes and penalties. So, while access is possible, it’s not always financially ideal. How to withdraw money from Fidelity 401k after leaving job? If you’ve left your job, you can withdraw funds, roll them over, or leave them invested. When considering how to withdraw money from Fidelity 401k after leaving job, keep in mind that early withdrawals may trigger a 10% penalty along with income taxes. How to withdraw money from Fidelity 401k before retirement without losing too much? If you're exploring how to withdraw money from fidelity 401k before retirement, the best approach is to check if you qualify for any penalty exceptions. Otherwise, early withdrawals usually come with taxes and additional charges, which can reduce your final amount. How to withdraw money from Fidelity 401k without penalty? You can avoid penalties if you are 59½ or older or qualify for specific IRS exceptions. Many people searching for how to withdraw money from fidelity 401k without penalty should focus on timing their withdrawal correctly or exploring structured withdrawal options. How to withdraw money from Fidelity 401k withdrawal online? The online process is simple. After logging in, go to your account dashboard, select the withdrawal option, and follow the instructions. This is what most people mean when they search for how to withdraw money from Fidelity 401k withdrawal online. How to cash out Fidelity 401k completely? If you’re looking at how to cash out fidelity 401k, you can withdraw the full balance from your account. However, this may result in taxes and penalties, especially if you're below retirement age. How to take money out of 401k Fidelity without withdrawing permanently? If you don’t want a permanent withdrawal, you can consider a loan. Many people exploring how to take money out of 401k fidelity find that loans offer temporary access without immediate tax penalties. How to take a loan from Fidelity 401k? To understand how to take a loan from fidelity 401k, log in to your account, check if your plan allows loans, choose the amount, and review repayment terms. Loan limits and conditions vary depending on your plan. How long does it take to receive money after withdrawal? Most withdrawals from Fidelity accounts are processed within 2–5 business days, depending on verification and the transfer method you select.

-

My everything bonus link promo codes send my gmail

Ytong877 replied to Dinudinkak's topic in Community Discussion

Mohu poprosit o nejake bonusove cody na muj email? -

Produktname – Jetterix Erfahrungen Nebenwirkungen – Keine nennenswerten Nebenwirkungen Kategorie – Gesundheit Ergebnisse – Innerhalb von 1–2 Monaten Verfügbarkeit – Online Bewertung: 5,0/5,0 (Jetterix Bewertungen und Beschwerden – ehrliche Analyse) Die sogenannte Jetterix Hochdruckdüse“ wird oft als revolutionäres Reinigungsgerät beworben, das Schmutz, Staub und Ablagerungen in Sekunden entfernen kann. Doch wie gut funktioniert dieses Produkt wirklich? In diesem ausführlichen Artikel werfen wir einen realistischen Blick auf Erfahrungen, Bewertungen, Vorteile und Beschwerden rund um Jetterix – basierend auf Nutzermeinungen, Produkttests und allgemeinen Erkenntnissen über Hochdruckdüsen. Offizielle Website https://www.fitprodiet.com/jetterix-erfahrungen/ https://www.instagram.com/p/DWGRobEk-pt/ https://www.instagram.com/p/DWGRzUtE820/ https://www.instagram.com/p/DWGR5ask4PF/ 1. Was ist Jetterix überhaupt? Jetterix Erfahrungen ist eine Hochdruckdüse, die an einen gewöhnlichen Gartenschlauch angeschlossen wird. Sie soll den Wasserdruck verstärken und so die Reinigung von Autos, Terrassen, Fenstern und Gartenmöbeln erleichtern. Grundsätzlich handelt es sich bei solchen Geräten um sogenannte Hochdruckdüsen – Zubehörteile, die Wasser mit erhöhter Geschwindigkeit ausstoßen, um Schmutz effizient zu entfernen. Besuchen Sie unsere Facebook-Seite und unsere Gruppen. https://www.facebook.com/JetterixErfahrungen/ https://www.facebook.com/groups/jetterix2026/ https://www.facebook.com/groups/jetterixtest/ https://www.facebook.com/groups/jetterixwirkung/ https://www.facebook.com/groups/jetterixwirkungundnebenwirkungen/ https://www.facebook.com/groups/jetterixprieskaufen/ https://www.facebook.com/groups/jetterixbewertungenundbeschwerden/ https://www.facebook.com/groups/jetterixbewertungen https://www.facebook.com/groups/jetterixoffiziellewebseite/ Typische Eigenschaften: Anschluss an Standard-Gartenschläuche Kein Strom notwendig Unterschiedliche Strahlmodi Leicht und tragbar 2. Jetterix Bewertungen – Was sagen Nutzer? Die Meinungen zu Produkten wie Jetterix oder ähnlichen „Jet-Nozzle“-Geräten sind sehr gemischt bis kritisch. Positive Bewertungen Einige Nutzer berichten: Einfache Anwendung ohne komplizierte Installation Praktisch für leichte Reinigungsarbeiten Ideal für Gartenbewässerung oder Staubentfernung Besonders bei: Fahrrädern Gartenmöbeln leichten Verschmutzungen wird die Leistung als ausreichend beschrieben. Jetterix Nozzle Pressure – Link zur offiziellen Website – Hier klicken Negative Bewertungen und Beschwerden Viele echte Erfahrungsberichte zeigen jedoch deutliche Schwächen: 1. Geringer Wasserdruck Mehrere Nutzer berichten, dass der Druck nicht stärker als ein normaler Gartenschlauch ist. 2. Übertriebene Werbung Ein häufiger Kritikpunkt: Werbevideos zeigen unrealistisch starke Leistung Oft wird ein echter Hochdruckreiniger im Hintergrund verwendet Ein Käufer schreibt: 3. Schlechte Qualität Einige Beschwerden: Billige Materialien Kurze Lebensdauer Undichte Verbindungen 4. Probleme mit Bestellung & Rückgabe Mehrere Nutzer berichten: falsche Liefermengen schwierige Rückerstattung zusätzliche Kosten (z. B. Zollgebühren) 5. Sehr schlechte Gesamtbewertung Einige Plattformen zeigen extrem niedrige Bewertungen: TrustScore nahe 1 von 5 Sternen für ähnliche Produkte Viele 1-Stern-Rezensionen 3. Warum funktioniert Jetterix oft nicht wie erwartet? Der wichtigste Punkt: Physikalische Grenzen Ein Gartenschlauch liefert begrenzten Druck. Eine Düse kann den Strahl formen – aber nicht den Wasserdruck stark erhöhen. Das bedeutet: Kein Ersatz für echte Hochdruckreiniger Nur optische Verstärkung des Strahls 4. Vergleich mit echten Hochdruckreinigern Professionelle Geräte: nutzen elektrische Pumpen erzeugen hohen Druck (100+ bar) reinigen effektiv selbst hartnäckigen Schmutz Normale Düsen wie Jetterix: arbeiten nur mit Leitungsdruck sind deutlich schwächer Tests zeigen, dass hochwertige Düsen zwar helfen können, aber echte Leistung von Geräten mit Motor kommt. 5. Vorteile von Jetterix Trotz Kritik gibt es einige Pluspunkte: ✔ Einfach zu benutzen Kein Strom, keine Installation ✔ Leicht & mobil Ideal für schnellen Einsatz ✔ Günstig Deutlich billiger als Hochdruckreiniger ✔ Vielseitig Gartenbewässerung leichte Reinigung Fenster abspülen 6. Nachteile von Jetterix Kein echter Hochdruck Hauptkritikpunkt Marketing oft irreführend Werbung verspricht mehr als geliefert wird Qualitätsprobleme Je nach Anbieter unterschiedlich Kundenservice oft schlecht Besonders bei Online-Shops 7. Für wen lohnt sich Jetterix? Geeignet für: leichte Reinigungsarbeiten Gartenpflege Nutzer mit kleinem Budget Nicht geeignet für: starke Verschmutzungen Autowäsche mit hartem Schmutz professionelle Reinigung 8. Tipps vor dem Kauf Wenn du überlegst, Jetterix Bewertungen zu kaufen: ✔ Bewertungen prüfen ✔ Rückgaberecht beachten ✔ Erwartungen realistisch halten ✔ Alternative Marken vergleichen 9. Alternative Lösungen Statt Jetterix könntest du überlegen: Hochwertige Gartendüsen bessere Verarbeitung verstellbare Strahlen Echte Hochdruckreiniger deutlich effektiver langfristig bessere Investition UNBEDINGT ANSEHEN: (EXKLUSIVES ANGEBOT) HIER KLICKEN FÜR PREISE & VERFÜGBARKEIT 10. Fazit – Jetterix Bewertungen & Beschwerden Jetterix Pries wirkt auf den ersten Blick wie ein praktisches Wundermittel – doch die Realität sieht anders aus. Zusammenfassung: Gute Idee, aber begrenzte Leistung Viele negative Bewertungen Werbung oft übertrieben Kein Ersatz für Hochdruckreiniger Endgültiges Urteil: Jetterix kann für einfache Aufgaben nützlich sein, aber wer echte Reinigungskraft erwartet, wird wahrscheinlich enttäuscht.

Produktname – Jetterix Erfahrungen Nebenwirkungen – Keine nennenswerten Nebenwirkungen Kategorie – Gesundheit Ergebnisse – Innerhalb von 1–2 Monaten Verfügbarkeit – Online Bewertung: 5,0/5,0 (Jetterix Bewertungen und Beschwerden – ehrliche Analyse) Die sogenannte Jetterix Hochdruckdüse“ wird oft als revolutionäres Reinigungsgerät beworben, das Schmutz, Staub und Ablagerungen in Sekunden entfernen kann. Doch wie gut funktioniert dieses Produkt wirklich? In diesem ausführlichen Artikel werfen wir einen realistischen Blick auf Erfahrungen, Bewertungen, Vorteile und Beschwerden rund um Jetterix – basierend auf Nutzermeinungen, Produkttests und allgemeinen Erkenntnissen über Hochdruckdüsen. Offizielle Website https://www.fitprodiet.com/jetterix-erfahrungen/ https://www.instagram.com/p/DWGRobEk-pt/ https://www.instagram.com/p/DWGRzUtE820/ https://www.instagram.com/p/DWGR5ask4PF/ 1. Was ist Jetterix überhaupt? Jetterix Erfahrungen ist eine Hochdruckdüse, die an einen gewöhnlichen Gartenschlauch angeschlossen wird. Sie soll den Wasserdruck verstärken und so die Reinigung von Autos, Terrassen, Fenstern und Gartenmöbeln erleichtern. Grundsätzlich handelt es sich bei solchen Geräten um sogenannte Hochdruckdüsen – Zubehörteile, die Wasser mit erhöhter Geschwindigkeit ausstoßen, um Schmutz effizient zu entfernen. Besuchen Sie unsere Facebook-Seite und unsere Gruppen. https://www.facebook.com/JetterixErfahrungen/ https://www.facebook.com/groups/jetterix2026/ https://www.facebook.com/groups/jetterixtest/ https://www.facebook.com/groups/jetterixwirkung/ https://www.facebook.com/groups/jetterixwirkungundnebenwirkungen/ https://www.facebook.com/groups/jetterixprieskaufen/ https://www.facebook.com/groups/jetterixbewertungenundbeschwerden/ https://www.facebook.com/groups/jetterixbewertungen https://www.facebook.com/groups/jetterixoffiziellewebseite/ Typische Eigenschaften: Anschluss an Standard-Gartenschläuche Kein Strom notwendig Unterschiedliche Strahlmodi Leicht und tragbar 2. Jetterix Bewertungen – Was sagen Nutzer? Die Meinungen zu Produkten wie Jetterix oder ähnlichen „Jet-Nozzle“-Geräten sind sehr gemischt bis kritisch. Positive Bewertungen Einige Nutzer berichten: Einfache Anwendung ohne komplizierte Installation Praktisch für leichte Reinigungsarbeiten Ideal für Gartenbewässerung oder Staubentfernung Besonders bei: Fahrrädern Gartenmöbeln leichten Verschmutzungen wird die Leistung als ausreichend beschrieben. Jetterix Nozzle Pressure – Link zur offiziellen Website – Hier klicken Negative Bewertungen und Beschwerden Viele echte Erfahrungsberichte zeigen jedoch deutliche Schwächen: 1. Geringer Wasserdruck Mehrere Nutzer berichten, dass der Druck nicht stärker als ein normaler Gartenschlauch ist. 2. Übertriebene Werbung Ein häufiger Kritikpunkt: Werbevideos zeigen unrealistisch starke Leistung Oft wird ein echter Hochdruckreiniger im Hintergrund verwendet Ein Käufer schreibt: 3. Schlechte Qualität Einige Beschwerden: Billige Materialien Kurze Lebensdauer Undichte Verbindungen 4. Probleme mit Bestellung & Rückgabe Mehrere Nutzer berichten: falsche Liefermengen schwierige Rückerstattung zusätzliche Kosten (z. B. Zollgebühren) 5. Sehr schlechte Gesamtbewertung Einige Plattformen zeigen extrem niedrige Bewertungen: TrustScore nahe 1 von 5 Sternen für ähnliche Produkte Viele 1-Stern-Rezensionen 3. Warum funktioniert Jetterix oft nicht wie erwartet? Der wichtigste Punkt: Physikalische Grenzen Ein Gartenschlauch liefert begrenzten Druck. Eine Düse kann den Strahl formen – aber nicht den Wasserdruck stark erhöhen. Das bedeutet: Kein Ersatz für echte Hochdruckreiniger Nur optische Verstärkung des Strahls 4. Vergleich mit echten Hochdruckreinigern Professionelle Geräte: nutzen elektrische Pumpen erzeugen hohen Druck (100+ bar) reinigen effektiv selbst hartnäckigen Schmutz Normale Düsen wie Jetterix: arbeiten nur mit Leitungsdruck sind deutlich schwächer Tests zeigen, dass hochwertige Düsen zwar helfen können, aber echte Leistung von Geräten mit Motor kommt. 5. Vorteile von Jetterix Trotz Kritik gibt es einige Pluspunkte: ✔ Einfach zu benutzen Kein Strom, keine Installation ✔ Leicht & mobil Ideal für schnellen Einsatz ✔ Günstig Deutlich billiger als Hochdruckreiniger ✔ Vielseitig Gartenbewässerung leichte Reinigung Fenster abspülen 6. Nachteile von Jetterix Kein echter Hochdruck Hauptkritikpunkt Marketing oft irreführend Werbung verspricht mehr als geliefert wird Qualitätsprobleme Je nach Anbieter unterschiedlich Kundenservice oft schlecht Besonders bei Online-Shops 7. Für wen lohnt sich Jetterix? Geeignet für: leichte Reinigungsarbeiten Gartenpflege Nutzer mit kleinem Budget Nicht geeignet für: starke Verschmutzungen Autowäsche mit hartem Schmutz professionelle Reinigung 8. Tipps vor dem Kauf Wenn du überlegst, Jetterix Bewertungen zu kaufen: ✔ Bewertungen prüfen ✔ Rückgaberecht beachten ✔ Erwartungen realistisch halten ✔ Alternative Marken vergleichen 9. Alternative Lösungen Statt Jetterix könntest du überlegen: Hochwertige Gartendüsen bessere Verarbeitung verstellbare Strahlen Echte Hochdruckreiniger deutlich effektiver langfristig bessere Investition UNBEDINGT ANSEHEN: (EXKLUSIVES ANGEBOT) HIER KLICKEN FÜR PREISE & VERFÜGBARKEIT 10. Fazit – Jetterix Bewertungen & Beschwerden Jetterix Pries wirkt auf den ersten Blick wie ein praktisches Wundermittel – doch die Realität sieht anders aus. Zusammenfassung: Gute Idee, aber begrenzte Leistung Viele negative Bewertungen Werbung oft übertrieben Kein Ersatz für Hochdruckreiniger Endgültiges Urteil: Jetterix kann für einfache Aufgaben nützlich sein, aber wer echte Reinigungskraft erwartet, wird wahrscheinlich enttäuscht. -

https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEioaTRUquxslKqvmabO3jG2WfucXhmwXV9Q9fzgHH4KASrh7-cUFKQXcpJK1QP3-buPkQV_jKZ6bND1WiT3zloQjds2Uo4fOXlF5oRAs43wb436mBG3HOeuORMJG2JN4PR3sVb7RIAgTxVj5F9p-BTyYEVCAgNCt2ofloL-3zMII15XYesHHXXzdgJJrEE/w640-h444/frert.PNG In der heutigen Zeit suchen immer mehr Menschen nach effizienten Lösungen, um Haus, Garten und Fahrzeuge schnell und gründlich zu reinigen. Eine innovative Option, die zunehmend Aufmerksamkeit erhält, ist die sogenannte Hochdruckdüse – wie sie beispielsweise unter dem Namen Jetterix vermarktet wird. Doch wie gut funktioniert dieses Produkt wirklich? Welche Erfahrungen berichten Nutzer, und gibt es Nebenwirkungen oder Risiken? Offizielle Website https://www.fitprodiet.com/jetterix-erfahrungen/ https://www.instagram.com/p/DWGRobEk-pt/ https://www.instagram.com/p/DWGRzUtE820/ https://www.instagram.com/p/DWGR5ask4PF/ In diesem ausführlichen Beitrag (ca. 2000 Wörter) erfährst du alles über Jetterix Erfahrungen, die Wirkung, die Vorteile sowie mögliche Nebenwirkungen – objektiv, verständlich und praxisnah erklärt. Jetterix Nozzle Pressure – Link zur offiziellen Website – Hier klicken Produktname – Jetterix Erfahrungen Nebenwirkungen – Keine nennenswerten Nebenwirkungen Kategorie – Gesundheit Ergebnisse – Innerhalb von 1–2 Monaten Verfügbarkeit – Online Bewertung: 5,0/5,0 Was ist Jetterix überhaupt? Jetterix ist im Grunde eine Hochdruck-Wasserdüse, die an einen normalen Gartenschlauch angeschlossen wird. Ziel ist es, durch gezielte Druckverstärkung eine kraftvolle Reinigung zu ermöglichen – ohne teure Hochdruckreiniger. Die Funktionsweise basiert auf einem simplen physikalischen Prinzip: Wasser wird durch eine verengte Düse gepresst Dadurch steigt die Geschwindigkeit des Wasserstrahls Das Ergebnis ist ein starker, fokussierter Wasserstrahl Ähnliche Systeme werden auch bei sogenannten Hydrojet-Anwendungen genutzt, bei denen Wasser gezielt Druck ausübt, um Effekte zu erzielen . Wie funktioniert die Wirkung von Jetterix? Die Wirkung lässt sich in drei Hauptbereiche unterteilen: 1. Mechanische Reinigungskraft Der konzentrierte Wasserstrahl löst: Schmutz Staub Schlamm Moos Diese Methode ist besonders effektiv bei: Terrassen Autos Fahrrädern Gartenmöbeln 2. Zeitersparnis Viele Nutzer berichten, dass sie deutlich schneller reinigen können als mit herkömmlichem Schlauchdruck. 3. Vielseitigkeit Durch verschiedene Sprühmodi kann Jetterix sowohl: sanft (z. B. Pflanzenbewässerung) als auch intensiv (z. B. hartnäckiger Schmutz) eingesetzt werden Jetterix Erfahrungen – Was sagen Nutzer? Da es sich nicht um ein medizinisches Produkt handelt, basieren Erfahrungen hauptsächlich auf Anwenderberichten und praktischer Nutzung. Positive Erfahrungen Viele Nutzer berichten: Einfache Installation Spürbar stärkerer Wasserstrahl Gute Ergebnisse bei leichten bis mittleren Verschmutzungen Günstige Alternative zu Hochdruckreinigern Ein häufig genannter Vorteil ist die Flexibilität im Alltag – besonders für kleinere Reinigungsarbeiten. Neutrale Erfahrungen Einige Nutzer sehen Jetterix eher als: Ergänzung, nicht Ersatz für Profi-Geräte praktische Lösung für gelegentliche Nutzung Negative Erfahrungen Kritische Stimmen berichten: Kein echter Hochdruck wie bei elektrischen Geräten Wirkung hängt stark vom Wasserdruck ab Bei starkem Schmutz begrenzte Leistung Wissenschaftlicher Blick auf die Wirkung Auch wenn Jetterix kein medizinisches Produkt ist, lässt sich seine Wirkung gut mit bekannten Wasserstrahl-Technologien vergleichen. Zum Beispiel zeigen Anwendungen wie die Hydrojet-Technologie, dass Wasserstrahlen: die Durchblutung fördern mechanische Reize auslösen gezielt Druck ausüben können Übertragen auf die Reinigung bedeutet das: Der Wasserstrahl wirkt wie eine physikalische Kraft, die Schmutzpartikel ablöst. Vorteile von Jetterix im Alltag 1. Kosteneffizienz Kein Strom erforderlich Günstiger als Hochdruckreiniger 2. Umweltfreundlich Nur Wasserverbrauch Keine Chemikalien nötig 3. Einfache Anwendung Anschluss an Standard-Gartenschlauch Sofort einsatzbereit 4. Platzsparend Kein sperriges Gerät Leicht zu verstauen Jetterix Wirkung im Detail Reinigung von Fahrzeugen Entfernt Staub und leichte Verschmutzungen Schonender als Bürsten Gartenreinigung Ideal für Wege, Fliesen und Möbel Entfernt Blätter und Schlamm Bewässerung Einstellbare Modi ermöglichen sanfte Pflanzenpflege Nebenwirkungen – Gibt es Risiken? Da Jetterix Erfahrungen kein medizinisches Produkt ist, gibt es keine klassischen Nebenwirkungen wie bei Medikamenten. Dennoch können indirekte Risiken oder Nachteile auftreten. 1. Verletzungsgefahr durch starken Wasserstrahl Ein sehr konzentrierter Wasserstrahl kann: Haut reizen kleine Verletzungen verursachen Vergleichbar mit anderen Wasserstrahl-Anwendungen kann intensiver Druck mechanische Reize erzeugen. 2. Materialschäden Zu hoher Druck kann: Lack beschädigen empfindliche Oberflächen angreifen 3. Abhängigkeit vom Wasserdruck Die Leistung hängt stark vom vorhandenen Wasserdruck ab: Bei niedrigem Druck → schwache Wirkung Bei hohem Druck → bessere Ergebnisse 4. Falsche Erwartungen Ein häufiger Kritikpunkt: Jetterix ersetzt keinen echten Hochdruckreiniger Gibt es echte Nebenwirkungen im medizinischen Sinne? Nein. Im Gegensatz zu medizinischen oder kosmetischen Anwendungen, bei denen Nebenwirkungen wie: Rötungen Schwellungen Schmerzen auftreten können handelt es sich bei Jetterix ausschließlich um ein mechanisches Reinigungsgerät. UNBEDINGT ANSEHEN: (EXKLUSIVES ANGEBOT) HIER KLICKEN FÜR PREISE & VERFÜGBARKEIT https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEj4HFA9RzHlb9Lb59xmuGP7U98dr7s12uuQeUQki8sKT4P6mALuK2NePX__h0jwDf6Zl6P6fP2UH-nuBjNVyK1KEzxF-U_-JxNfqNAKIHp_3TlAaLNqOzl5Amv9_lk_FyVBAG1xZP_oIfnNOZbazzBRqvwgSLEYnhb0Xh5N1yBae-feVBEBh-AcWJMOF94/w640-h640/adsfrgr.PNG Für wen ist Jetterix geeignet? Ideal für: Hausbesitzer Gartenliebhaber Autobesitzer Menschen, die schnelle Reinigung wollen Weniger geeignet für: Industrielle Reinigung Extrem hartnäckige Verschmutzungen Professionelle Anwendungen Anwendungstipps für beste Ergebnisse 1. Richtigen Wasserdruck nutzen Optimal: mittlerer bis hoher Leitungsdruck 2. Abstand beachten Nicht zu nah an empfindliche Oberflächen 3. Richtigen Modus wählen Sanft für Pflanzen Stark für Schmutz 4. Regelmäßige Reinigung Verhindert Ablagerungen und verbessert Wirkung Vergleich: Jetterix vs. Hochdruckreiniger Merkmal Jetterix Hochdruckreiniger Preis Günstig Teuer Strombedarf Nein Ja Druckleistung Mittel Sehr hoch Mobilität Hoch Eingeschränkt Einsatzbereich Alltag Profi/Heavy Duty Fazit: Jetterix ist eine praktische Alltagslösung, aber kein Ersatz für Profi-Geräte. Häufige Fragen (FAQ) Ist Jetterix wirklich effektiv? Ja – besonders bei leichten bis mittleren Verschmutzungen. Kann es gefährlich sein? Nur bei falscher Anwendung (z. B. zu hoher Druck auf Haut oder empfindliche Materialien). Gibt es Nebenwirkungen? Keine klassischen Nebenwirkungen – nur mechanische Risiken bei falscher Nutzung. Lohnt sich der Kauf? Für viele Haushalte: Ja, besonders als günstige Alternative. Fazit: Jetterix Erfahrungen im Gesamtbild Jetterix Bewertungen ist eine smarte, praktische und kostengünstige Lösung für alltägliche Reinigungsaufgaben. Die Erfahrungen zeigen: Vorteile: einfache Anwendung gute Reinigungsleistung im Alltag vielseitig einsetzbar Nachteile: kein Ersatz für Hochdruckreiniger abhängig vom Wasserdruck Nebenwirkungen: keine medizinischen Risiken nur mechanische Vorsicht notwendig Gesamtbewertung: Jetterix Pries eignet sich ideal für alle, die eine schnelle, unkomplizierte Reinigungslösung suchen – ohne großen Aufwand oder hohe Kosten. Besuchen Sie unsere Facebook-Seite und unsere Gruppen. https://www.facebook.com/JetterixErfahrungen/ https://www.facebook.com/groups/jetterix2026/ https://www.facebook.com/groups/jetterixtest/ https://www.facebook.com/groups/jetterixwirkung/ https://www.facebook.com/groups/jetterixwirkungundnebenwirkungen/ https://www.facebook.com/groups/jetterixprieskaufen/ https://www.facebook.com/groups/jetterixbewertungenundbeschwerden/ https://www.facebook.com/groups/jetterixbewertungen https://www.facebook.com/groups/jetterixoffiziellewebseite/

-

I was reading some discussions about electric off-road karts and saw people mentioning the 1000 Watt Electric Mud Monster Dallas Power Sports when comparing electric options for trail riding. The 1000W setup seems to be a solid choice for riders who want decent power without going into gas engines. A lot of people like electric karts because they’re quieter and easier to maintain. They also seem great for casual riding where noise or fuel isn’t ideal. It’s interesting seeing how more riders are starting to consider electric karts alongside traditional gas models.

I was reading some discussions about electric off-road karts and saw people mentioning the 1000 Watt Electric Mud Monster Dallas Power Sports when comparing electric options for trail riding. The 1000W setup seems to be a solid choice for riders who want decent power without going into gas engines. A lot of people like electric karts because they’re quieter and easier to maintain. They also seem great for casual riding where noise or fuel isn’t ideal. It’s interesting seeing how more riders are starting to consider electric karts alongside traditional gas models. -

When managing retirement savings, knowing how to withdraw money from a Fidelity 401k is essential for financial flexibility. Whether you are planning for retirement, facing an emergency, or have recently left your job, we must understand the correct withdrawal methods, tax implications, and penalty rules. A Fidelity 401k withdrawal allows you to access your retirement funds under specific conditions. These withdrawals can be completed online, through the Fidelity platform, or via direct assistance. The key is choosing the right withdrawal type based on your situation. How to Withdraw Money from Fidelity 401k Online We can easily complete a Fidelity 401k withdrawal online by following a structured process. This is the fastest and most convenient method. Step-by-Step Process 1. Log in to your Fidelity account 2. Navigate to the Retirement Accounts section 3. Select your 401k plan 4. Click on Withdrawals or Loans 5. Choose your withdrawal type 6. Enter the amount and confirm details 7. Submit your request Once submitted, funds are typically transferred via direct deposit or check, depending on your preference. How to Withdraw Money from Fidelity 401k After Leaving a Job After leaving employment, your options expand significantly. We can access funds in several ways: · Cash out the 401k · Roll over to an IRA · Transfer to a new employer’s plan If we choose to cash out Fidelity 401k after leaving a job, the process is straightforward, but it may come with taxes and penalties. A rollover, however, allows us to preserve retirement savings without immediate tax consequences. How to Withdraw Money from Fidelity 401k Rollover Accounts A Fidelity 401k rollover occurs when funds are moved into an IRA or another retirement account. If you need to withdraw from a rollover account: · Log in to your rollover account · Select withdrawal options · Choose between partial or full distribution · Confirm tax withholding preferences Withdrawals from rollover accounts are treated similarly to traditional 401k withdrawals and may be subject to income tax and penalties if taken early. How to Withdraw Money from Fidelity 401k Before Retirement Accessing funds before age 59½ requires careful planning. Early withdrawals are allowed, but they typically come with: · 10% early withdrawal penalty · Federal and state income taxes However, we can avoid penalties in certain situations: · Financial hardship withdrawals · Qualified medical expenses · Permanent disability · Substantially equal periodic payments (SEPP) Understanding these exceptions helps us minimize financial loss when accessing funds early. How to Withdraw Money from Fidelity 401k Without Penalty To withdraw money from Fidelity 401k without penalty, we must meet specific criteria. Some of the most common penalty-free scenarios include: · Reaching age 59½ · Leaving your job at age 55 or older (Rule of 55) · Using funds for qualified hardship expenses · Taking required minimum distributions (RMDs) after age 73 By planning withdrawals strategically, we can reduce or eliminate penalties entirely. How to Cash Out Fidelity 401k If we decide to cash out a Fidelity 401k, the process involves withdrawing the entire balance. This option provides immediate access to funds but has significant financial consequences. Key Considerations · Full balance becomes taxable income · Possible 10% early withdrawal penalty · Loss of future retirement growth Despite these drawbacks, cashing out may be necessary in urgent financial situations. How to Take Money Out of Fidelity 401k Safely When we take money out of a Fidelity 401k, the goal is to minimize losses. The safest approach includes: · Withdrawing only what is needed · Understanding tax implications · Choosing the correct withdrawal type · Considering a rollover instead of cashing out This ensures we maintain long-term financial stability. How to Take a Loan from Fidelity 401k Instead of withdrawing funds, we can consider a 401k loan from Fidelity. This allows us to borrow money without triggering taxes or penalties. Key Features of a 401k Loan · Borrow up to 50% of your vested balance · Maximum loan limit of $50,000 · Repayment period typically 5 years · Interest paid back into your account A loan is often a better alternative because it preserves retirement savings while providing liquidity. How to Take a Loan from Fidelity 401k Online Taking a loan is simple: 1. Log in to your Fidelity account 2. Select your 401k plan 3. Click on Loans and Withdrawals 4. Choose Loan Option 5. Enter loan amount and repayment terms 6. Submit your request Funds are usually disbursed quickly, making this a practical option for short-term financial needs. Tax Implications of Fidelity 401k Withdrawals Every Fidelity 401k withdrawal comes with tax considerations. We must account for: · Federal income tax withholding (usually 20%) · Additional state taxes · Potential penalty fees Proper planning ensures we avoid unexpected tax burdens and retain more of our savings. Best Strategies to Minimize Taxes and Penalties To maximize our withdrawal efficiency, we should: · Use rollovers instead of cash withdrawals · Withdraw funds after age 59½ · Utilize hardship exemptions when eligible · Spread withdrawals over multiple years to reduce tax brackets These strategies help us maintain control over our retirement funds. Final Thoughts Understanding how to pull money out of Fidelity 401k is crucial for making informed financial decisions. Whether we choose a withdrawal, rollover, or loan, each option carries its own advantages and consequences. By carefully evaluating our situation, we can access funds when needed while protecting long-term financial security.

-

Lipojaro Gotas: Guia Completo sobre o Suplemento para Emagrecimento Site Oficial : https://www.kissnutra.com/pt/lipojaro-gotas/ https://soundcloud.com/aryan-miglani-267981311/lipojaro-onde-comprar-guia https://scribehow.com/page/LipoJaro_para_Emagrecimento_Beneficios_Efeitos_e_Suporte_Metabolico__v_JPQscnQpiEC4kMBGs7wA https://scribehow.com/page/LipoJaro_Ingredientes_e_Beneficios_Pilula_Dietetica_para_Perda_de_Peso__vGSccPZRR2qH6CVKCctKew https://open.firstory.me/story/cmmw0bk7r01ug01z84d8813a6 Nos últimos anos, a busca por soluções eficazes para perda de peso tem crescido significativamente. Com rotinas cada vez mais aceleradas, muitas pessoas encontram dificuldade em manter uma alimentação equilibrada e uma prática regular de exercícios físicos. Nesse contexto, surgem suplementos naturais que prometem auxiliar no emagrecimento de forma prática e segura. Entre esses produtos, o LipoJaro no Brazil tem ganhado destaque. Neste artigo, vamos explorar em detalhes o que é o Lipojaro Gotas, como funciona, seus ingredientes, benefícios, modo de uso, possíveis efeitos colaterais e outras informações importantes para quem está considerando utilizar esse suplemento. Facebook: https://www.facebook.com/lipojarogotas/ https://www.facebook.com/lipojarogotas2026/ https://www.facebook.com/groups/lipojarogotas/ https://www.facebook.com/groups/lipojarogotasglpparaperdadepeso/ https://www.facebook.com/groups/lipojaroparaemagrecimento/ https://www.facebook.com/groups/lipojarocomprar/ https://www.facebook.com/groups/lipojaroingredientes/ https://www.facebook.com/groups/lipojarogotasoferta/ https://www.facebook.com/groups/lipojarovantagens/ https://www.facebook.com/groups/lipojaroefeitoscolaterais/ Pinterest: https://in.pinterest.com/pin/978547825301584843 https://in.pinterest.com/pin/978547825301584884 https://in.pinterest.com/pin/1116892776362181256 https://in.pinterest.com/pin/1116892776362181299 Videos: https://www.youtube.com/watch?v=0Eq453PoNSc https://www.dailymotion.com/video/xa2b4ac https://slaps.com/track/pGhBpvFT https://vimeo.com/1174723335 https://soundcloud.com/aryan-miglani-267981311/lipojaro-onde-comprar-guia https://videa.hu/videok/felnott/lipojaro-aplicaes-e-emagrecimento-como-8YjSFS1pxAWj13Sg https://soundcloud.com/aryan-miglani-267981311/lipojaro-em-farmacias-onde Leia também: https://differ.blog/p/lipojaro-para-emagrecimento-benef-cios-efeitos-e-suporte-metab-lico-5fa98c https://hackmd.io/@TIOvfZBzR0GrV6ZRvFaUVw/lipojarogotas https://groups.google.com/g/lipojaro-gotas/c/LXmixdqwTTE https://impact-fitness-studio.blogspot.com/2026/03/lipojaro-efeitos-colaterais-e-seguro.html https://medium.com/@lipojarogotas/lipojaro-em-farm%C3%A1cias-onde-comprar-com-melhor-pre%C3%A7o-02c26edd4eca https://lipojarogotas.blogspot.com/2026/03/lipojaro-ingredientes-e-beneficios.html https://hackmd.io/@TIOvfZBzR0GrV6ZRvFaUVw/lipojarogotasComprar Também em: https://www.kissnutra.com/de/lipojaro-erfahrungen/ #LipoJaro #LipoJaroGotas #LipoJaroAvaliações #LipoJaroGotasAvaliações #LipoJaroGLP #LipoJaroPerdaDePeso #LipoJaroEmagrecimento #LipoJaroPreço #LipoJaroComprar #LipoJaroIngredientes #LipoJaroPílulaDietética #LipoJaroOferta #LipoJaroVantagens #LipoJaroFunciona #LipoJaroAnvisa #LipoJaroConfiável #LipoJaroAlternativa #LipoJaroWegovy #LipoJaroBenefícios #LipoJaroEfeitosColaterais #LipoJaroBrasil #LipoJaroFarmácias #LipoJaroEfeitos #LipoJaroAplicações #LipoJaroSuporteMetabólico #LipoJaroSuplementos #LipoJaroSiteOficial #LipoJaroOndeComprar

Lipojaro Gotas: Guia Completo sobre o Suplemento para Emagrecimento Site Oficial : https://www.kissnutra.com/pt/lipojaro-gotas/ https://soundcloud.com/aryan-miglani-267981311/lipojaro-onde-comprar-guia https://scribehow.com/page/LipoJaro_para_Emagrecimento_Beneficios_Efeitos_e_Suporte_Metabolico__v_JPQscnQpiEC4kMBGs7wA https://scribehow.com/page/LipoJaro_Ingredientes_e_Beneficios_Pilula_Dietetica_para_Perda_de_Peso__vGSccPZRR2qH6CVKCctKew https://open.firstory.me/story/cmmw0bk7r01ug01z84d8813a6 Nos últimos anos, a busca por soluções eficazes para perda de peso tem crescido significativamente. Com rotinas cada vez mais aceleradas, muitas pessoas encontram dificuldade em manter uma alimentação equilibrada e uma prática regular de exercícios físicos. Nesse contexto, surgem suplementos naturais que prometem auxiliar no emagrecimento de forma prática e segura. Entre esses produtos, o LipoJaro no Brazil tem ganhado destaque. Neste artigo, vamos explorar em detalhes o que é o Lipojaro Gotas, como funciona, seus ingredientes, benefícios, modo de uso, possíveis efeitos colaterais e outras informações importantes para quem está considerando utilizar esse suplemento. Facebook: https://www.facebook.com/lipojarogotas/ https://www.facebook.com/lipojarogotas2026/ https://www.facebook.com/groups/lipojarogotas/ https://www.facebook.com/groups/lipojarogotasglpparaperdadepeso/ https://www.facebook.com/groups/lipojaroparaemagrecimento/ https://www.facebook.com/groups/lipojarocomprar/ https://www.facebook.com/groups/lipojaroingredientes/ https://www.facebook.com/groups/lipojarogotasoferta/ https://www.facebook.com/groups/lipojarovantagens/ https://www.facebook.com/groups/lipojaroefeitoscolaterais/ Pinterest: https://in.pinterest.com/pin/978547825301584843 https://in.pinterest.com/pin/978547825301584884 https://in.pinterest.com/pin/1116892776362181256 https://in.pinterest.com/pin/1116892776362181299 Videos: https://www.youtube.com/watch?v=0Eq453PoNSc https://www.dailymotion.com/video/xa2b4ac https://slaps.com/track/pGhBpvFT https://vimeo.com/1174723335 https://soundcloud.com/aryan-miglani-267981311/lipojaro-onde-comprar-guia https://videa.hu/videok/felnott/lipojaro-aplicaes-e-emagrecimento-como-8YjSFS1pxAWj13Sg https://soundcloud.com/aryan-miglani-267981311/lipojaro-em-farmacias-onde Leia também: https://differ.blog/p/lipojaro-para-emagrecimento-benef-cios-efeitos-e-suporte-metab-lico-5fa98c https://hackmd.io/@TIOvfZBzR0GrV6ZRvFaUVw/lipojarogotas https://groups.google.com/g/lipojaro-gotas/c/LXmixdqwTTE https://impact-fitness-studio.blogspot.com/2026/03/lipojaro-efeitos-colaterais-e-seguro.html https://medium.com/@lipojarogotas/lipojaro-em-farm%C3%A1cias-onde-comprar-com-melhor-pre%C3%A7o-02c26edd4eca https://lipojarogotas.blogspot.com/2026/03/lipojaro-ingredientes-e-beneficios.html https://hackmd.io/@TIOvfZBzR0GrV6ZRvFaUVw/lipojarogotasComprar Também em: https://www.kissnutra.com/de/lipojaro-erfahrungen/ #LipoJaro #LipoJaroGotas #LipoJaroAvaliações #LipoJaroGotasAvaliações #LipoJaroGLP #LipoJaroPerdaDePeso #LipoJaroEmagrecimento #LipoJaroPreço #LipoJaroComprar #LipoJaroIngredientes #LipoJaroPílulaDietética #LipoJaroOferta #LipoJaroVantagens #LipoJaroFunciona #LipoJaroAnvisa #LipoJaroConfiável #LipoJaroAlternativa #LipoJaroWegovy #LipoJaroBenefícios #LipoJaroEfeitosColaterais #LipoJaroBrasil #LipoJaroFarmácias #LipoJaroEfeitos #LipoJaroAplicações #LipoJaroSuporteMetabólico #LipoJaroSuplementos #LipoJaroSiteOficial #LipoJaroOndeComprar -